Everyone chasing the AI trade buys Nvidia. But the real choke point may be a dull one.

It is the job of moving data inside a data center. One small chipmaker just doubled its growth forecast for exactly that.

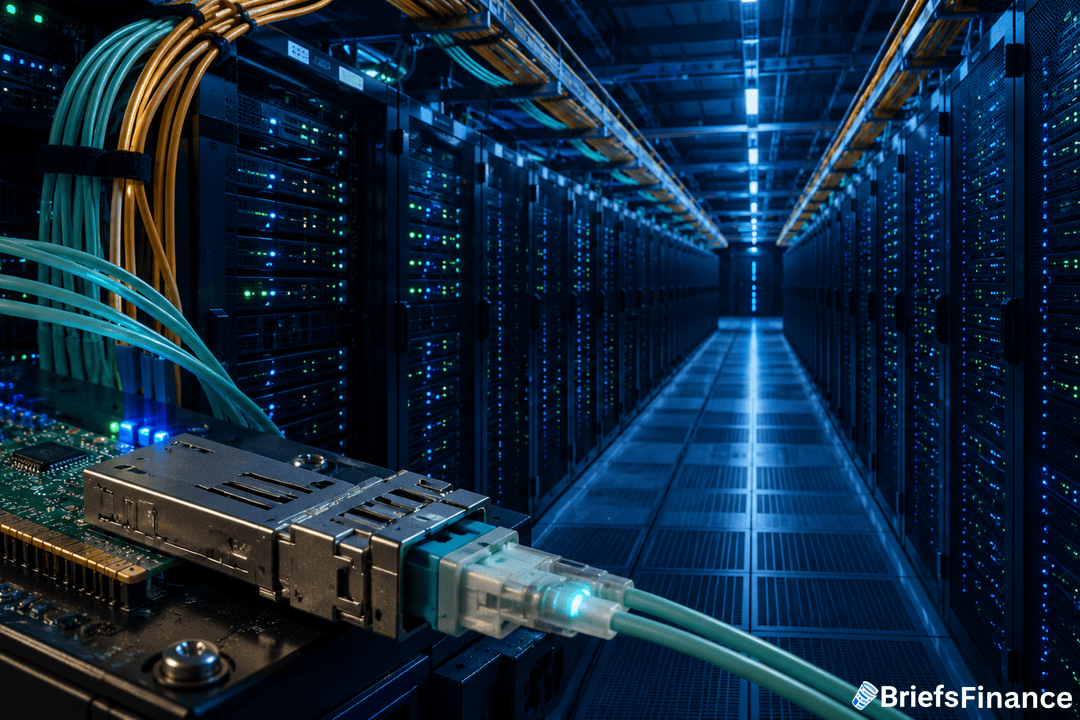

The Company Behind The Wires

MACOM trades under the ticker MTSI. It makes the optical parts that move data inside data centers.

Picture them as the on-ramps and lanes that AI traffic drives through. AI needs huge data centers to run.

Those centers move a flood of data. MACOM's parts help it move fast.

Optical parts turn data into light and back. Light moves faster than copper wires.

The AI boom runs on more than brains. It runs on plumbing too, and MACOM sells the pipes.

The firm raised its 2026 data-center growth target from 35% to over 60%. It now sees total sales growing about 30% for the year.

Last quarter, sales hit $289 million. That was up about 22% from a year earlier.

Adjusted profit came in at $1.09 per share. Earnings per share is just profit split across every share of stock.

We break down the AI names Wall Street is actually buying, not just the obvious ones, in Market Briefs, plus a free investing masterclass when you join.

Why Wall Street Noticed

The clearest tell is the order book. MACOM booked $1.50 of new orders for every $1 it shipped.

Its backlog is now at a record. That ratio is called book-to-bill.

Anything above 1 means demand is beating supply. Right now demand is clearly winning.

A record backlog means orders are stacking up. The firm just has to build and ship them.

Josh Brown of Ritholtz Wealth added MACOM to his CNBC "Best Stocks in the Market" list on June 18. He called it a name right at the heart of the data-center buildout.

The stock jumped about 22% after its last update. Investors clearly liked the new outlook.

Small chip names like this often fly under the radar. A doubled forecast is hard to ignore.

Growth that fast tends to draw a crowd. Big funds are starting to take notice.

Most of the AI hype still goes to the chip makers. The parts that link those chips get far less notice.

That gap is where MACOM lives. And it is not all AI either.

It still gets steady demand from defense and satellite buyers. That mix gives it more than one way to grow.

What To Watch

For this quarter, MACOM guided to sales of $331 million to $339 million. It also sees gross margins near 60%.

Those fat margins leave plenty of room for profit to grow. That is rare for a parts maker.

The big question is whether it can keep filling that record backlog. When orders run this far ahead of shipments, the next few quarters usually tell the story.

Sign up for Market Briefs to get moves like this every morning in five minutes, with a 45-minute investing course thrown in for free.