A $107 billion loss year sounds like a bad one.

In 2025, it counted as the calm one.

That is the part that should get an investor's attention.

Why A Calm Year Was Still A $100 Billion Year

Global insured losses from disasters hit $107 billion in 2025. That was down from $141 billion the year before, a Swiss Re report found.

The drop had a simple cause. No major hurricane hit the U.S. coast.

Take that luck away, and the bill snaps back up. Even so, 2025 was the sixth straight year over $100 billion.

The floor keeps rising, even in the quiet years. Swiss Re's sigma report expects about $148 billion in a normal 2026.

So the calm was a break, not a fix. The trend still points up.

We connect big news to your money in Market Briefs, delivered each morning with a free investing masterclass when you join.

Follow The Money Up The Chain

Insurers buy their own insurance. It is called reinsurance, and its price flows down to your bill.

When global losses are huge, reinsurance gets pricey. Your premium then follows it up.

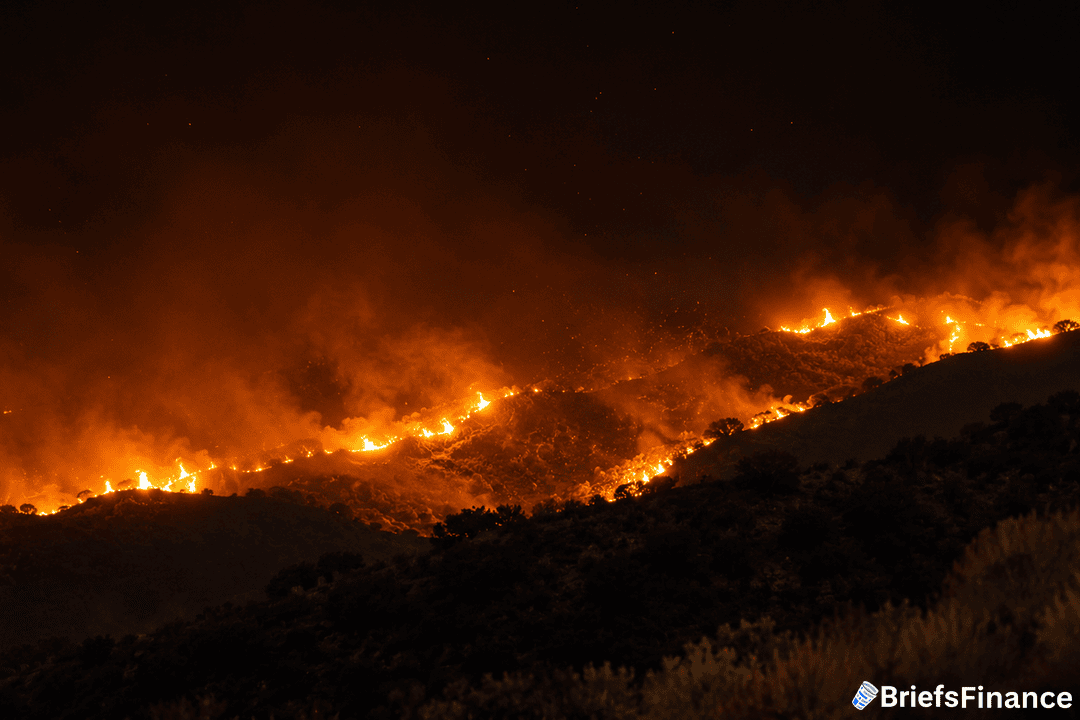

The Los Angeles wildfires drove much of 2025. They caused about $40 billion in insured losses in January, a record for any wildfire.

The cost to rebuild adds a second push. Labor, materials, and tariffs all got pricier, so every claim costs more.

It all feeds back into the housing market. Pricier coverage makes pricier homes, even when the loan gets cheaper.

The Floor Got Reset

Reinsurance prices actually softened a bit in 2025. That is why 2026 hikes are expected to be smaller.

But the bottom has moved up. Even calm years now start at a higher number.

What Drove The Losses

The mix of damage is shifting. Wildfires, storms, and floods drove a record 92% of 2025 losses.

Severe storms alone cost about $51 billion. Wildfire is the fastest-growing risk of all.

It is rising about 12% a year. That pace reshapes how insurers price the West.

For the first time, about half of all disaster losses were insured. That is a record share.

It sounds like progress. But it also means insurers are on the hook for more.

Earthquakes and big hurricanes stayed quiet in 2025. That quiet will not last forever.

By 2030, losses could reach $186 billion. That is if the trend simply holds.

None of this shows up in your loan. It shows up in your premium.

So the cost of risk keeps climbing on its own track. The Fed has no say over it.

The pattern is clear enough. Risk is spreading to more states each year.

That widens the map insurers must cover. And a wider map costs more to insure.

Worth Noting

One quiet year does not undo six loud ones. The risk did not go anywhere.

If you want the market explained like a friend would, join Market Briefs. Five minutes a day, plus a 45-minute investing course as a bonus.