For years, builders were the ones who held the land.

Not anymore. Now Wall Street holds it.

A new Bloomberg report pegs PGIM at $4 billion in US land bank deals.

PGIM is the asset arm of Prudential Financial. It runs $1.4 trillion in assets.

The deals are part of a bigger push into asset-based finance, or ABF.

ABF is a way of lending where the loan is backed by a pool of real assets, in this case lots that builders will buy back to build on.

It's a quiet part of private credit. And it just got loud.

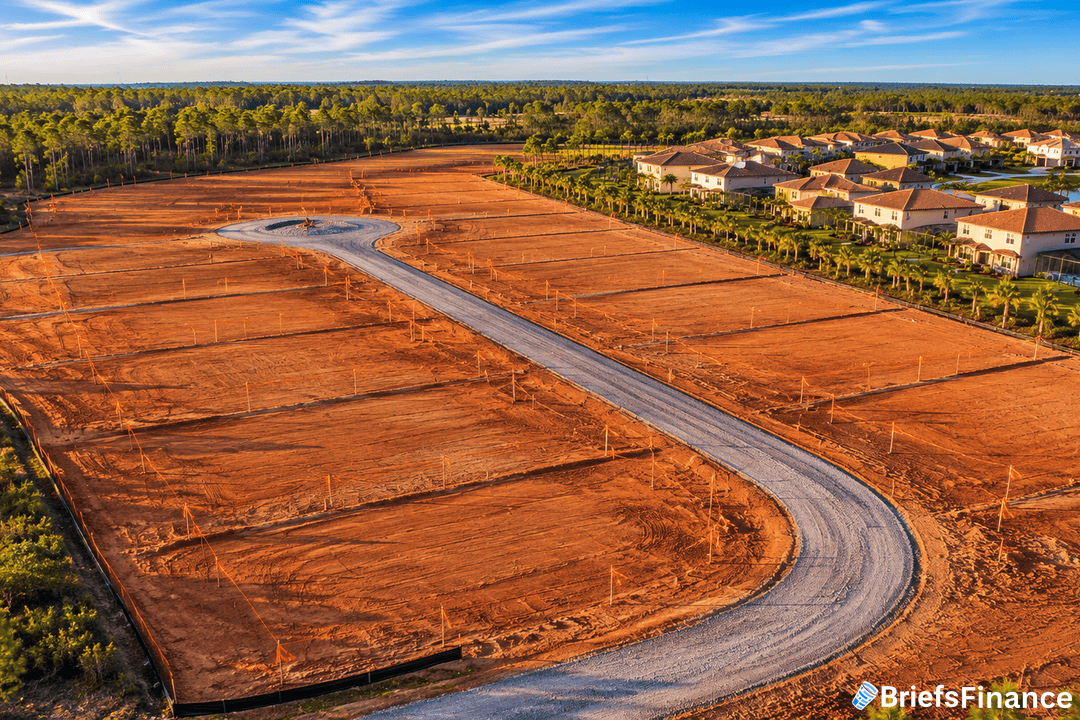

Why Builders Pay Wall Street To Hold Their Land

Holding land is costly. It eats cash and earns nothing until homes go up.

Builders would rather rent the land than own it, which is where PGIM steps in.

A land banker buys the lot, holds it for a few years, then sells it back to the builder.

The builder pays a fee for the option but skips the full cost of holding the land.

For PGIM, the deals offer steady income at a time when bond yields look weak.

For builders, it's a way to keep building while mortgage rates stay high.

Housing starts are down. Buyers are scarce. But the long-term math still says the US needs more homes.

Land banking is the bet that the math wins out.

Market Briefs breaks down stories like this in five minutes. A free 45-minute investing class comes with it when you join.

PGIM Is Not The Only Buyer

PGIM is just the latest big name in line.

Last week, Guggenheim launched its own platform with Bedrock Land Finance. Guggenheim runs $362 billion in assets.

The pitch was nearly the same. Help builders stay "asset-light" while Wall Street holds the dirt.

Walton Global is also raising a $250 million fund. It targets returns of up to 11.5% on land-backed loans.

PGIM has been busy in ABF too. It bought $500 million of Affirm's loans, then grew the deal to up to $3 billion in 2025. It wants $500 billion in private assets within five years.

The trend reflects a broader shift on Wall Street. Banks have pulled back from this kind of lending, and asset managers have stepped in to fill the gap.

Bank rules tied to past crashes pushed lenders out of this space. Private credit funds, with fewer rules, moved in.

What To Watch

Land banking is no longer a fix. It's now its own asset class.

The next test comes when housing slows. These deals last years, the lots are hard to sell, and the plan only works if builders buy the land back.

If housing demand holds, this is a steady cash flow play for big asset firms.

If it doesn't, the land on Wall Street's books becomes their problem to fix.

PGIM's $4 billion bet says they think housing demand will hold up just fine. Time will tell if they got it right.

If you want this kind of read every weekday, join Market Briefs. A 45-minute investing course comes with it as a bonus.