For 15 years, community banks have been forced to follow rules written for giant lenders. But a bank in a small town does not have the same resources as a Wall Street giant. Michelle Bowman, a former community banker herself, says that mismatch is hurting local lending.

She delivered that message at the Kansas City Fed's conference, which was hosted by President Schmid. Her audience was community bankers - the very people who deal with these burdens every day.

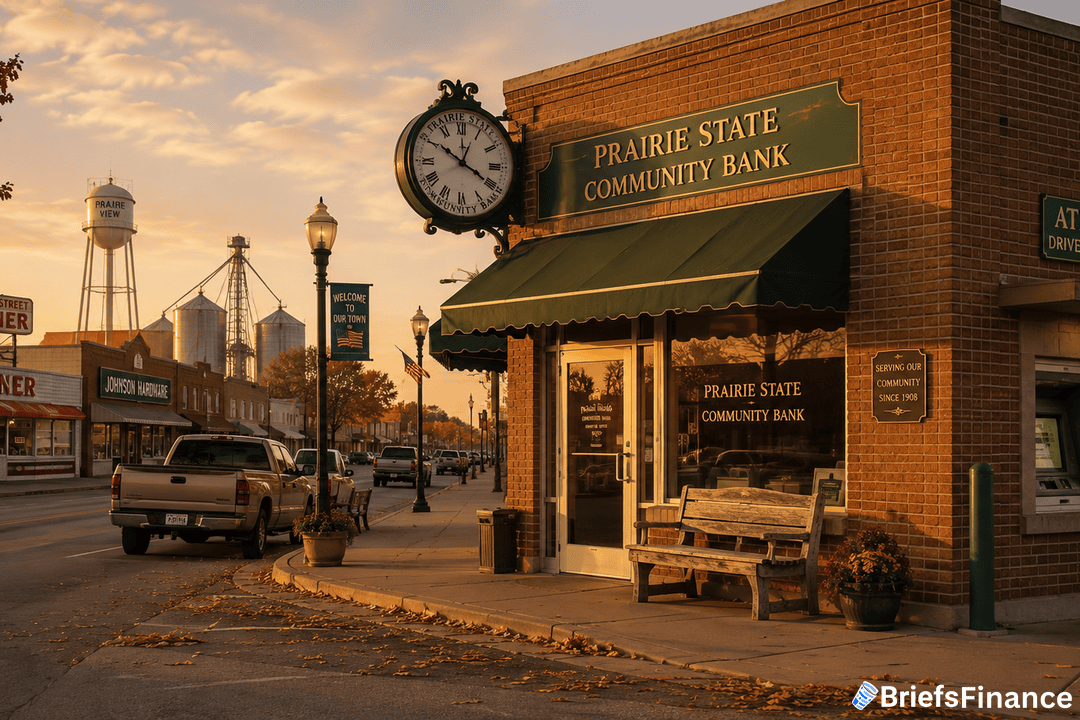

Bowman's perspective is informed by her own experience as a community banker before joining the Federal Reserve. She has consistently advocated for tailored regulations that recognize the distinct business models of smaller lenders. The 10th District, which includes states like Kansas, Missouri, Nebraska, and Oklahoma, is heavily dependent on these banks for agricultural and small business lending.

Two Rules That Squeeze Small Lenders

Bowman pointed to two specific rules that create unfair pressure. The first is the CECL accounting rule. CECL stands for "Current Expected Credit Losses." It requires banks to build complex models to predict future loan losses. For a community bank that makes simple loans to local farmers and small businesses, that kind of modeling is overkill.

Get your free investing masterclass bonus when you join Market Briefs, our free daily newsletter

The second rule is Regulation O, which governs loans to bank insiders - like directors or their families. Bowman said examiners have penalized minor mistakes in this area. As a result, many community banks have simply banned all insider credit. That hurts local relationships and makes it harder for community banks to serve their boards and local leaders.

The regulations were designed with massive, intricate financial institutions and their extensive compliance departments in mind. Bowman said, "Applying them to a 639-bank district where most are rural is like forcing a bicycle to follow tractor-trailer regulations." It slows everything down.

A New Direction for Supervision

Bowman said the Fed plans to shift its focus. Instead of checking every small procedural mistake, supervisors will concentrate on material financial risks - the things that could really harm a bank's health. She also mentioned that the Fed recently finalized changes to the community bank leverage ratio. That ratio is a simplified way for small banks to measure their capital strength, and the changes give them more flexibility.

On technology, Bowman said the Fed will work to understand and support emerging tools like artificial intelligence, digital assets, and new payment systems. Community banks need to adopt these if they want to compete, and the Fed wants to help - not block them with more big-bank rules.

What to Watch

The Fed's promise to tailor supervision for community banks is not new, but Bowman's speech shows a clear push to follow through. The next step will be seeing whether examiners on the ground actually change their approach. For now, community banks have a strong voice in Washington - and that voice is asking for a simpler, fairer rulebook.

Subscribe to Market Briefs, our free daily newsletter, and claim your bonus investing masterclass