GFL Environmental is considering going private. But its $7.1 billion debt pile makes that hard. Investors love its steady cash flow from trash collection. That is the tension: a valuable asset with a heavy load.

The Deal in Play

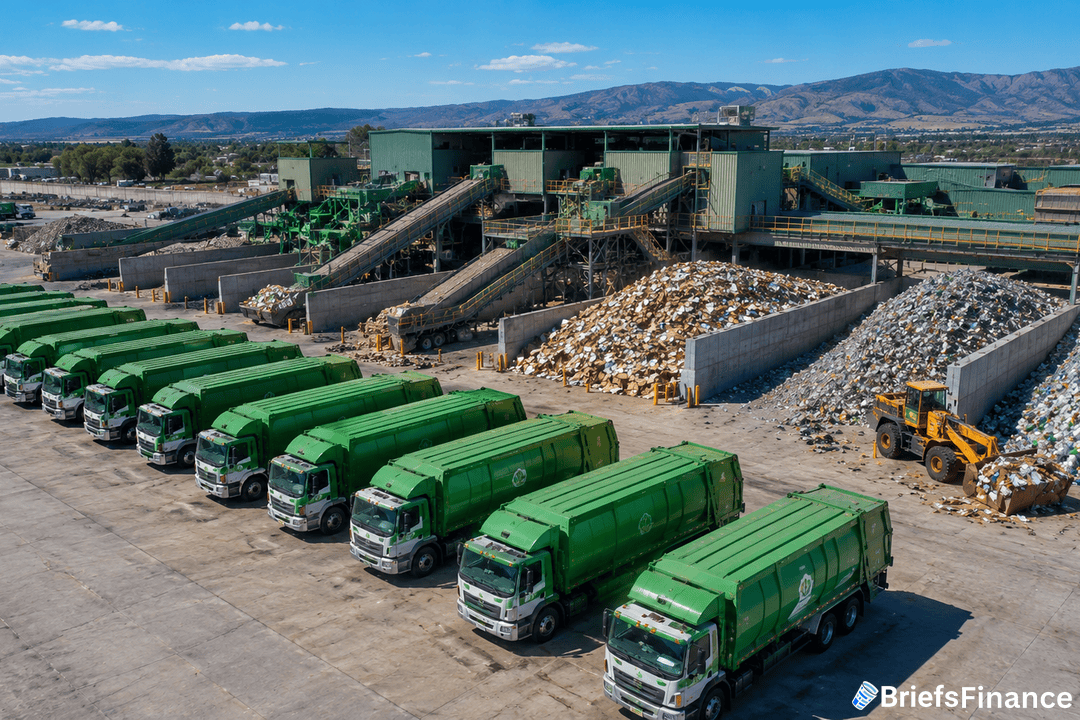

GFL Environmental Inc. is a waste-management company that describes itself as the "fourth-largest diversified" environmental services firm in North America. It was founded in 2007. In recent months, buyout firms showed preliminary interest in taking the company private. Management started talking to advisers about possible options.

A "take-private" means a company buys back all its public stock and becomes privately owned. Any buyer would need founder and CEO Patrick Dovigi to keep his stake. Without him, the deal likely falls apart.

Some suitors might instead buy a minority stake - a small ownership share that does not give full control. The talks are early and may not lead to a deal.

Get your free investing masterclass bonus when you join Market Briefs, our free daily newsletter

Why Investors Want GFL

Environmental services companies are attractive because they have steady recurring revenue and reliable cash flow. Think of GFL like a garbage truck that picks up cash every month - it never stops. This steady stream allows firms to consolidate more businesses, buying up smaller rivals to grow.

In 2025, Apollo Global Management Inc. teamed up with BC Partners, both buyout firms, to buy a controlling interest in GFL's environmental services division. That same year, Energy Capital Partners purchased a minority stake in GFL's road-building and construction unit, called Green Infrastructure Partners. That unit was valued at C$4.25 billion ($3 billion) in the deal. These moves show investors already value parts of the company.

GFL's total market value after its stock rose on July 3, 2026, was C$20.7 billion ($14.6 billion). The jump came from the news of buyout interest.

The Other Moves

GFL is also working on a combination with Secure Waste Infrastructure Corp. to expand in Western Canada. That deal could happen alongside or separate from a take-private. The company recently moved its executive headquarters from Ontario to Miami Beach, Florida. That shift may signal a focus on U.S. investors or a different tax structure.

Any buyer would need to handle GFL's $7.1 billion debt. That is a big number - like trying to buy a house with a huge mortgage already on it. The debt could make a full buyout tough. But the steady cash flow might help a buyer pay it down over time.

What to Watch

Talks are still early and may fall apart. Some firms may just buy a minority stake instead of going all in. The combination with Secure Waste also moves forward. For now, GFL stays public.

Subscribe to Market Briefs, our free daily newsletter, and claim your bonus investing masterclass