Three weeks ago, Bolivia placed its first international bond in four years, and demand was five times the size of the offer.

Today that same bond is the worst-performing sovereign debt in emerging markets, after protests pushed the country's recovery story into reverse before the ink dried.

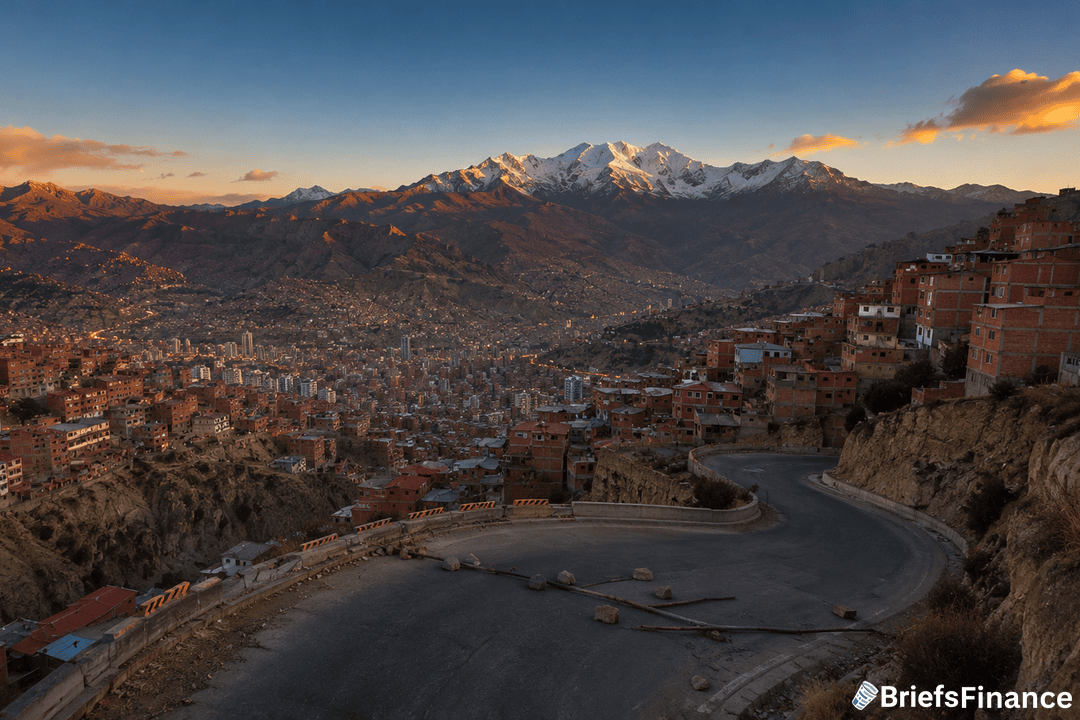

How A Victory Lap Turned Into A Selloff

Bolivia raised $1 billion on May 7 at a 9.45% yield, with 166 international buyers lining up and no domestic state funds buying out of obligation, which Economy Minister Jose Gabriel Espinoza framed as proof that markets believed in President Rodrigo Paz's reform push.

Then the protests started, with roadblocks going up across the country in early May as Indigenous groups, miners, and labor unions began demanding Paz resign six months into his term.

Former president Evo Morales has since joined in, leading a 190-kilometer march on the capital that has added political weight to what started as a protest over wages and a land law.

The bonds have dropped almost five cents on the dollar in two weeks, sending the 2031 notes to a 10.5% yield from 9.75% at issuance - a 75 basis point move in three weeks, which is a sprint for sovereign bonds.

For a five-minute morning read on how political risk like this actually moves your money, Market Briefs breaks it down every weekday, plus a free investing masterclass when you sign up.

What's Actually Driving The Protests

The unrest began as separate complaints, with some groups asking for higher wages, others protesting a land law, and farmers angry about contaminated fuel that had damaged thousands of vehicles.

Paz repealed the land law and offered teachers a bonus, but Indigenous groups kept pushing - blockading La Paz to force his resignation, with more than 3,500 roadblocks now scattered across the country and over 5,000 trucks stranded on highways.

The deeper issue is that Paz won the election with a centrist message and votes from working-class Bolivians, then cut the tax on big fortunes, hired business elites into his cabinet, and started talking to the IMF - reversals his base now treats as betrayal.

For investors with exposure to the region, the broader emerging market ETFs have been catching the spillover this month.

What To Watch

Paz's risk premium has already retraced most of its earlier gains, and if the blockades continue and food shortages deepen in La Paz, the bond selloff will get worse before it gets better.

A bond that prints with 5x demand and bleeds out in three weeks is a reminder of what frontier debt actually is.

Join 350,000+ investors reading Market Briefs every weekday morning - you also get a free 45-minute investing course as a bonus.