Homes hit a price record while rates climbed. That's the worst mix for spring buyers. It's like fighting gravity twice at once.

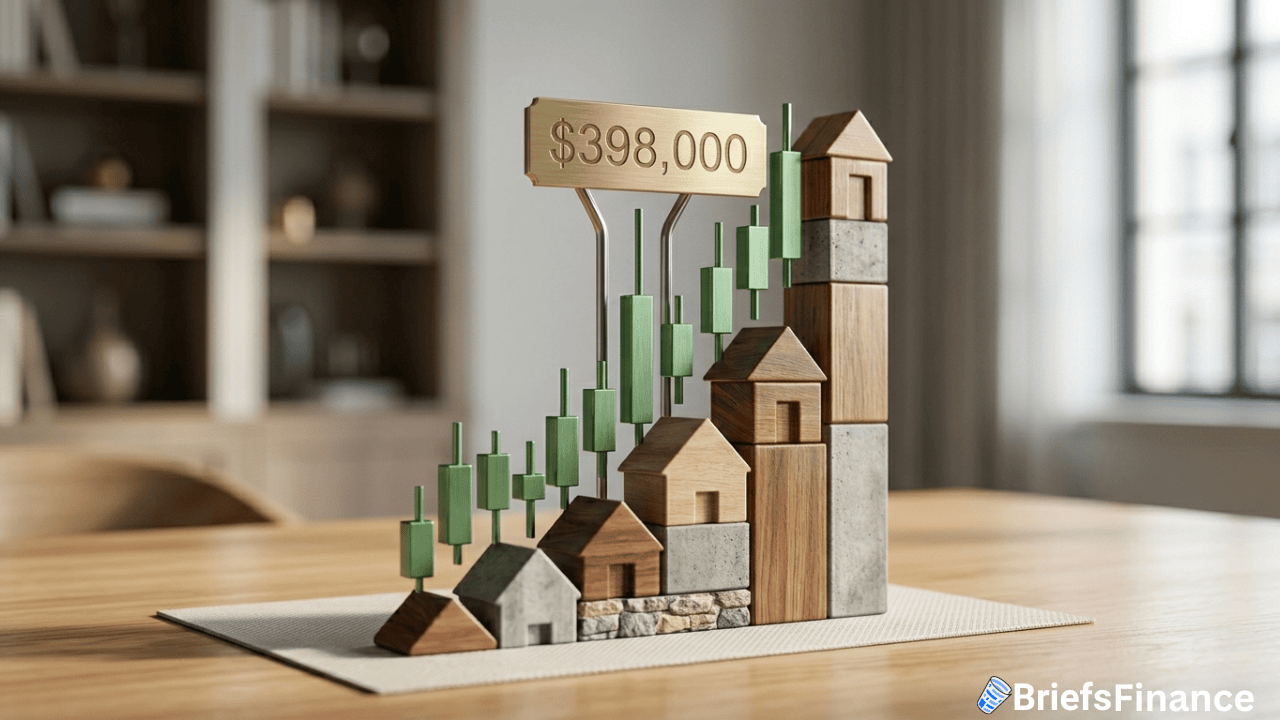

The February median home price was $398,000 - the highest ever on record. Meanwhile, the 30-year mortgage rate jumped to 6.46% in early April.

Oil Prices Pushing Rates Up

Oil near $100 per barrel worries the market about rising prices. The 10-year Treasury yield is the highest since last fall, pushing mortgage rates up with it.

The Iran war created inflation risk that didn't exist six months ago. Rates were supposed to fall. Buyers were supposed to get cheaper loans. Instead, the opposite happened.

It's a shock that hits just as spring buying begins.

Buyers Get Squeezed Both Ways

A $398,000 house at 6.46% costs far more monthly than a $380,000 house at 6.0%. The difference is hundreds of dollars per month. Over 30 years, that's tens of thousands in extra interest.

First-time buyers get hit hardest. They can barely afford loans at all. Higher rates and higher prices push many out entirely.

What to Watch

Watch mortgage application numbers weekly. If April applications fall, the spring season is broken.

Watch what the Fed says. If Fed leaders hint at keeping rates high because of prices, mortgage rates could jump more.

The ideal - low prices and low rates - isn't here. Buyers face the worst of both.