Mortgage rates were supposed to fall this year. Instead, they keep going the wrong direction.

The average 30-year fixed rate hit 6.46% this week - up from 6.38% a week ago and the highest level in nearly seven months. That makes it five weeks in a row of climbing rates, and it lands right in the middle of what's supposed to be the busiest stretch of the year for home sales.

The War Premium

A big part of the problem is coming from overseas. The conflict in Iran has sent energy prices sharply higher, and that's feeding back into inflation worries across the economy.

Those worries are pushing up yields on U.S. Treasury bonds - the benchmark that mortgage lenders use to set their rates. When bond yields rise, so do the rates borrowers pay.

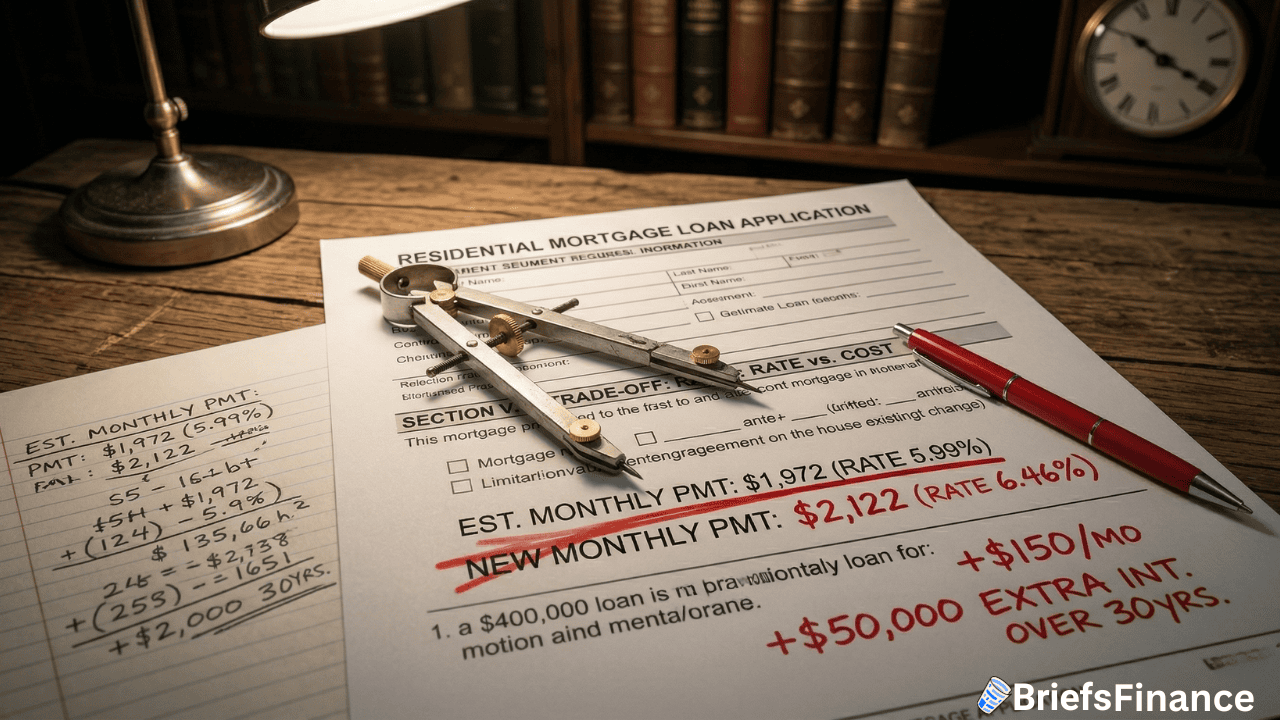

Just six weeks ago, rates had fallen into the high 5% range. For buyers who were running the numbers at that level, today's rates tell a very different story.

A borrower looking at a $400,000 loan would pay roughly $150 more per month at 6.46% than they would have in late February. That's like adding a car payment on top of your mortgage - and over 30 years, it adds up to more than $50,000 in extra interest.

Buyers Are Pulling Back

Overall mortgage applications fell more than 10% last week, according to the Mortgage Bankers Association.

Refinances got hit hardest - down 17% week over week and off more than 40% from where they stood a month ago. With rates marching higher, fewer homeowners see a reason to swap their current loan for a new one.

On the purchase side, applications dipped about 3%. That smaller drop likely reflects the fact that inventory has been improving - fresh listings rose over 20% between February and March, outpacing the typical seasonal bump.

But more supply only helps if buyers can afford to act. And right now, that math is getting harder.

What to Watch

Capital Economics already had a negative outlook on 2026 home sales. This week, they cut their forecast even further - specifically because of the recent spike in rates and the uncertainty around the war.

AI-related job worries aren't helping either. Between spiking energy costs and growing anxiety about automation, buyer confidence is getting squeezed from multiple sides.

Last spring, that kind of early-season energy vanished quickly once the economic outlook darkened. The housing market is staring at that same risk right now.