- A core-satellite portfolio splits investments into stable core holdings and higher-risk satellite picks.

- The core is usually 60% of the portfolio, with satellites at 40%.

- It blends passive index investing with active opportunity bets.

Producers in West Texas are paying buyers to haul off their natural gas. Factories in Germany are paying record prices for the same thing.

The Iran war just split the global gas market into two systems. Buyers trying to play this need to know which one they are standing in.

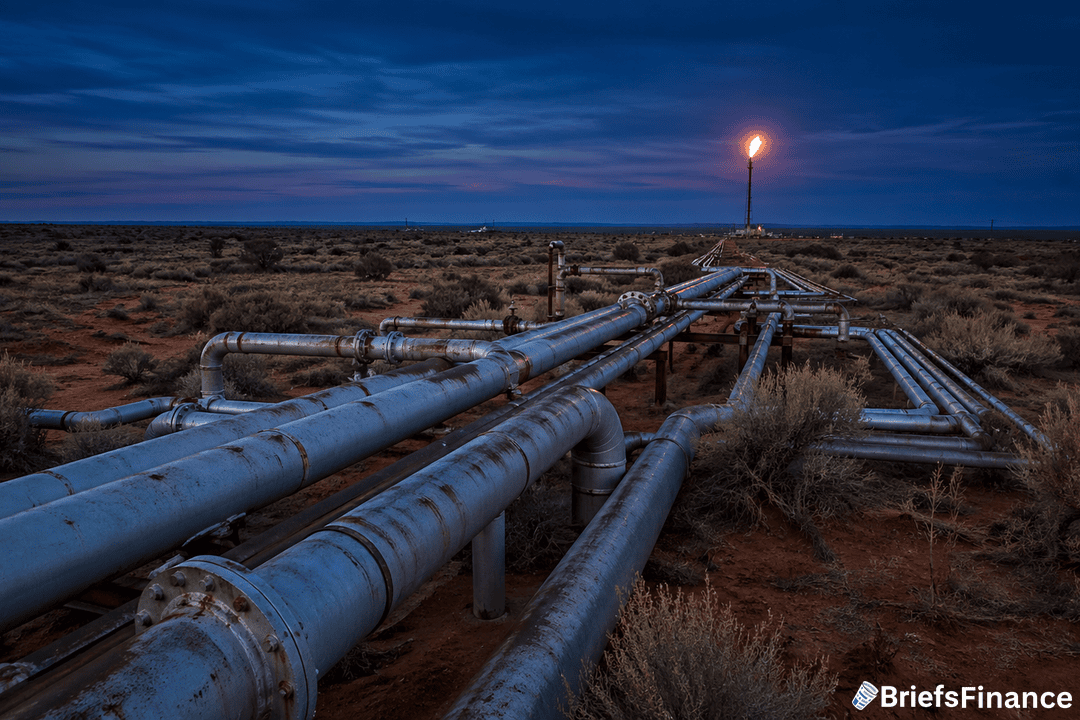

The Permian Basin in West Texas pumps a huge amount of natural gas. Most of it comes up as a byproduct of pumping oil. The pipelines that move that gas to anywhere useful are full.

Cash prices at Waha Hub, the regional benchmark, have been negative for 44 days in a row. They hit a record low of -$9.53 per MMBtu on April 15.

What does that mean in plain English? Producers are paying buyers to haul their gas off. They want to keep pumping the oil sitting under it.

Henry Hub, the national U.S. benchmark, is trading near $3. It is also at a premium to futures. The U.S. simply has more gas than it can move or use. LNG export ports cannot load fast enough to ship the surplus overseas.

Europe is in the opposite spot. The continent's main gas point, the TTF benchmark, nearly doubled to over €60/MWh by mid-March.

The cause is mostly geographic. About 20% of the world's LNG comes from Qatar and the UAE. Both of those flows ship through the Strait of Hormuz. Shipping there has slowed to a near standstill since the strikes on February 28.

Europe's storage is also tighter than usual. Tanks held 46 billion cubic meters at the end of February. That is down from 60 last year and 77 the year before. Refilling those tanks for next winter just got a lot more costly.

The split is creating very different chances on each side of the Atlantic.

In the U.S., midstream pipeline firms that own Permian capacity are getting paid to move gas at top rates. Anyone with a contract to load LNG at Gulf Coast export ports is also booking a strong margin.

In Europe, power firms and gas-heavy plants are getting squeezed on every cubic meter. Some are likely to lean back into coal as a substitute. That is most likely in Germany.

Asian buyers are also in the mix. They are competing with Europe for the same flexible LNG cargoes that used to flow from the Gulf. That bidding war is part of why TTF doubled.

The split has consumer effects too. U.S. household gas bills are likely to stay low this year. European bills will not.

About 4.5 Bcf/d of new pipeline capacity is set to come online in the Permian later this year. That should drag Waha Hub out of negative ground. It should also let more gas reach U.S. LNG export ports.

Hormuz is not running on a U.S. infrastructure timeline. The U.S. price problem will likely fix itself by year end. The European one is tied to a war.