The global luxury home market is doing something it hasn't done in a while. It's outpacing the rest of housing.

Prime property prices across 100 major cities grew faster than mainstream home prices last year, with Dubai and Tokyo leading the climb by a wide margin. The money chasing those markets has a story behind it - wealth migration, favorable tax codes, and a shrinking list of places the ultra-rich feel safe parking assets.

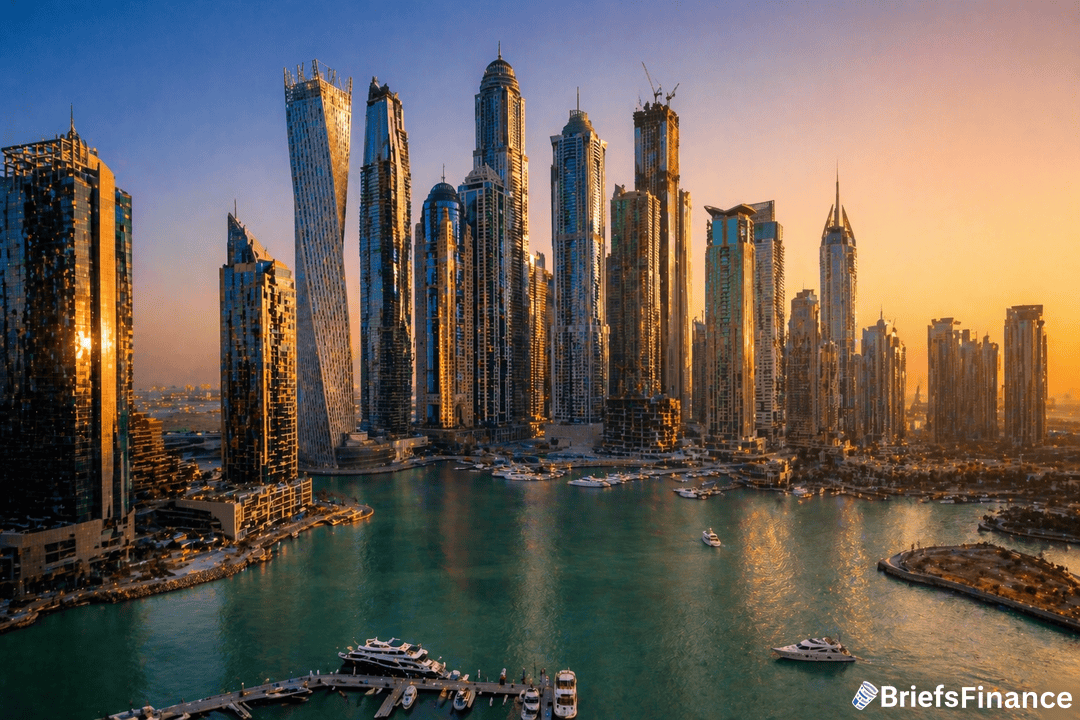

Where Prices Jumped The Most

Knight Frank tracks prime residential prices in 100 markets worldwide, and the benchmark rose 3.2% in 2025, ahead of the 2.9% gain in the mainstream market. The gap is small in percentage terms but meaningful in signal - high-end buyers are still writing checks while the rest of the market cools under higher rates and affordability pressure.

Dubai is the global standout. Prices there climbed 25% in 2025 and are now up roughly 200% over the past five years.

That's a move that would draw bubble warnings in most markets. In Dubai, it's being driven by inbound wealth from Russia, India, and the broader Middle East, plus an aggressive residency program that lets wealthy buyers become long-term residents through property purchases.

Tokyo delivered a 58% jump in 2025, the biggest single-year gain in the top 100. Mumbai, Brisbane, Miami, and Hong Kong are named as the next markets to watch, each for different reasons ranging from infrastructure buildouts to domestic wealth creation.

The US Picture Is Softer But Steady

The US luxury threshold, defined as the entry price for the top 10% of homes, was $1.25 million in March. That's down 2.9% from a year earlier but up 3.7% from February, which suggests luxury pricing softened over the past year and firmed again heading into spring.

The US luxury market is more regional than global luxury - local economies, state tax policy, and climate exposure drive performance more than cross-border capital flows. Vero Beach, Florida offers the tighter local story.

Homes priced above $1 million have seen sales jump 48.8% since the pandemic, with just 1.6% of that inventory currently sitting on the market. Supply is thin.

Demand is consistent. That combination keeps prices firm even as the rest of Florida housing has cooled.

The scale point: Vero Beach's tight inventory is a small version of what's happening in Dubai and Tokyo at a much larger scale. Limited supply plus sustained demand equals sustained price growth.

The Tax Code Is Driving Destinations

Where wealthy buyers choose to park money now has more to do with tax policy than weather or lifestyle. Miami, Milan, and Dubai are pulling capital in because they offer favorable tax treatment for residents and foreign buyers.

New York and London still carry strong lifestyle appeal but are losing market share to cities with cleaner tax setups. That shift matters for investors because it tells you where construction, commercial real estate, and luxury retail development are likely to follow.

Wealth migrations are slow-moving, but once they start, they tend to reinforce themselves - better restaurants follow the money, which attracts more money, which justifies more development.

What To Watch

Interest rates and currency moves are the biggest near-term variables for global luxury. A weaker dollar makes US markets cheaper for foreign buyers and tends to lift Miami and New York.

A stronger dollar flips the math. For Dubai and Tokyo, domestic demand is the bigger driver, so watch local economic data rather than US Treasury yields.

Longer term, tax policy changes in Europe and the US could accelerate or slow the current wealth migration trend. Any major shift in estate taxes, wealth taxes, or residency programs would reshape the winners and losers in this market.