Most owners losing their homes right now have a low loan rate.

That should be a shield. It is not. The bills around the house are doing what the loan cannot.

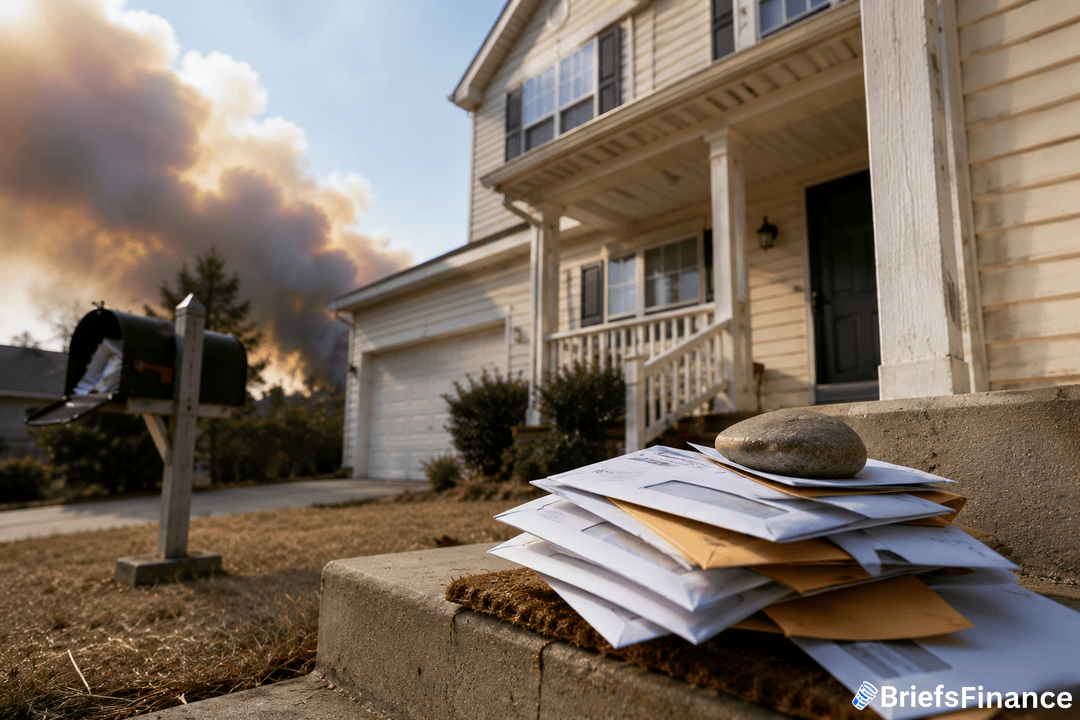

Insurance And Taxes Are The Real Squeeze

About 119,000 US homes got foreclosure filings in the first quarter. That is the highest count since early 2020, per data from real estate firm Attom that was first cited by The Wall Street Journal.

The number is up 26% from a year ago. It also lines up with where things sat before the pandemic, after relief plans paused most filings in 2020.

What is driving it is the kicker. Average home insurance jumped to $2,948 in 2025, up 12% from a year earlier, per a report from insurance site Insurify.

Property tax bills rose another 3% to an average of $4,427, Attom found. Add in HOA dues, the fees owners pay to live in some neighborhoods, and the math starts to break.

Even owners locked in safely at a 3% loan rate are feeling the pinch.

The hit is sharper in states where home values have run hot. Insurance prices in storm and fire zones have climbed every year since 2022.

Some big carriers have pulled out of states like Florida and California. That has pushed more owners into pricier state-backed plans, which adds to the monthly bill.

Owners in those zones now spend more on insurance than on the loan itself in many cases.

New Buyers Are More Exposed

Buyers who got homes in the past few years are in worse shape.

They locked in higher loan rates near 7%. In some markets, home values have slipped back, leaving a slice of those owners owing more than the home is worth.

That is the kind of setup that can turn a missed payment into a full default fast.

The relief options have shrunk too. The Federal Housing Administration said in October that owners can only use loan modification, a tool to lower monthly payments, once every 24 months.

That is a tighter window than the one in place during the pandemic. Back then, broad pause plans let owners skip payments with no near-term hit.

Those plans are gone, which means more owners now have to sell or face foreclosure.

What To Watch

The full mortgage market is also showing the strain.

The average monthly payment on every US mortgage hit $2,005 in the fourth quarter, a record high, per Realtor.com data.

That figure pulls in a huge group of borrowers locked in at 4% or lower. The jump is more striking with that base in place.

For investors, the read is simple. Home insurance and tax costs are now a bigger threat to owners than loan rates.

That shifts the risk for housing names, regional banks, and home services stocks tied to the same buyers.

Foreclosure activity is back to where it sat before COVID. The bills around the home are higher than they have ever been.