Tesla (TSLA) reported first-quarter 2026 results after the bell on Tuesday and posted a clear earnings beat. The company made $0.41 per share, topping the $0.37 Wall Street expected, while gross margin bounced back to 21.1% from 16.3% a year earlier.

Normally, numbers like that would send the stock sharply higher. Shares barely moved, which tells you the market is no longer grading Tesla on the core car business alone.

What the Beat Looked Like

Revenue came in at $22.39 billion, a 14% jump from the same quarter last year. That marks Tesla's first year-over-year revenue growth in several quarters, which is a real positive for a company that has spent 2025 shrinking on top-line.

Automotive margins, the number Wall Street analysts watch most closely, expanded more than they have in over a year. Even so, revenue missed the $22.64 billion figure analysts had modeled, and deliveries landed about 7,600 units below the 365,645 consensus.

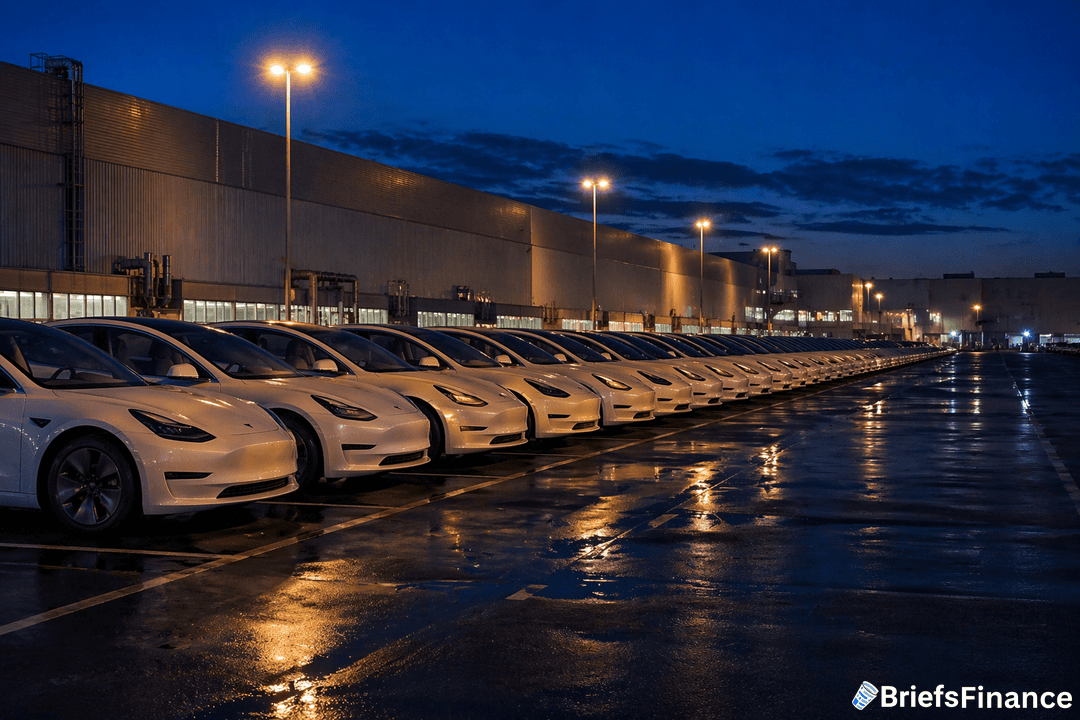

Why the Stock Stayed Flat

There is a clear gap between what Tesla sold and what it built in the quarter. The company produced more than 50,000 cars that did not get delivered, and that inventory build is the kind of demand warning sign investors watch for.

Energy storage, one of the bright spots in recent quarters, fell 38% from Q4 2025 to just 8.8 gigawatt-hours. That is well below the 12 to 14 gigawatt-hour range analysts had been modeling into their numbers.

The bigger issue: Bloomberg called the market reaction "cooling AI hype," since the Optimus, Robotaxi, and Full Self-Driving stories that powered shares last year now face tougher competition from Chinese robotaxi players and other humanoid-robot companies.

The China Factor

Tesla's China business remains a key swing factor for earnings, since local competitors like BYD and Xiaomi keep pulling share at lower price points. Q1 China revenue was mentioned only briefly on the call, which is rarely a bullish sign.

Analysts also flagged that the promised lower-priced model has slipped again, with management pointing to "later this year" rather than a firm date. Without that product, volume upside is capped through 2026.

What to Watch

Shareholder questions submitted through Say.com centered on Optimus v3, FSD milestones, and when the lower-priced "better than a minivan" vehicle launches. Until Tesla puts clearer timelines on those products, earnings beats may keep landing with a shrug.

Watch the cash flow statement next quarter, because with 50,000 unsold cars, Tesla is financing inventory on the balance sheet. Any further demand softness would hit cash before it hits the income statement.

Also worth watching: whether Tesla trims production to clear inventory or pushes deeper discounts into Q2. Either move would help volume but cut into the same margin recovery that just drove the Q1 beat.

Investors are now paying Tesla for two stories at once, and the company has to keep both alive through the second half.