A car loan is the most basic piece of middle-class debt, and it is the one breaking first.

Subprime auto delinquencies are running at their highest level since 1994, with a record number of borrowers more than 60 days behind on their payments. That is happening while household debt sits at a record $18.8 trillion.

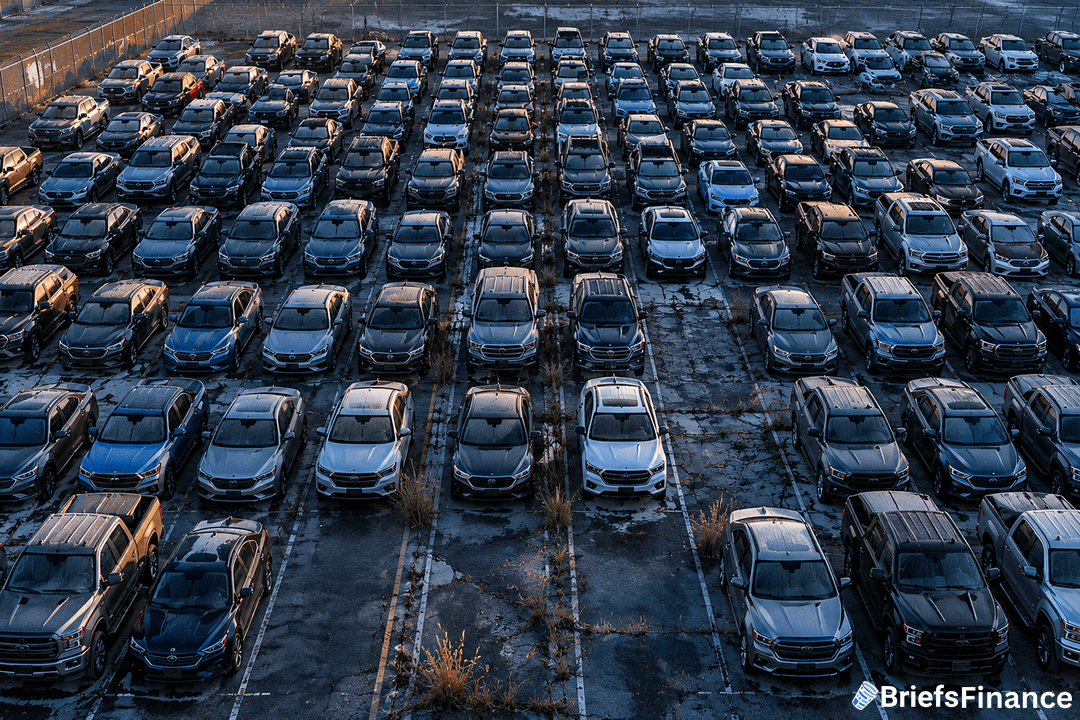

How Tight The Car Market Got

Americans now owe a record $1.68 trillion on auto loans, roughly even with the $1.69 trillion outstanding in federal student debt.

The average monthly payment on a new car is roughly $680, up almost 40% from 2018, while J.D. Power pegs the real average closer to $760. For borrowers stretched into loans longer than seven years, that payment can eat up about 20% of their monthly income.

The pain is heaviest at the bottom, with subprime borrowers falling behind at a rate not seen in three decades, per CarEdge data based on Fitch ratings.

Every weekday morning, Market Briefs breaks down credit signals like this one in plain English - five minutes a day, plus a free investing masterclass with the sign-up.

Why Payments Got So Big

New car prices started climbing in 2021 when chip shortages choked inventory, and they never really came back down.

The average new car now sells for about $50,000, about 30% higher than in 2019, while used car prices are still 29% above pre-pandemic levels per FRED. Automakers also leaned away from cheap models during the pandemic and toward pricier ones, which pulled the market further from buyers earning less.

Cox Automotive data shows the shift, with only 37% of new-car shoppers last year earning under six figures (down from 50% in 2020), while the share earning over $200,000 jumped from 18% to 29%.

In English: the new-car market is a K, and a lot of borrowers are on the wrong leg of it.

The Mortgage Side Is Cracking Too

Auto loans are not the only place stress is showing up.

The New York Fed reported that 4.8% of all household debt was in some stage of delinquency at the end of Q4 2025, with early-stage mortgage delinquencies rising. The damage is centered in lower-income areas and places where home prices are falling.

"Delinquency rates for mortgages are near historically normal levels, but the deterioration is concentrated in lower-income areas and in areas with declining home prices," said Wilbert van der Klaauw, an economic research advisor at the New York Fed.

The catch: a car repo or a missed mortgage hits harder than a credit card default, since more than three-quarters of Americans rely on a car to get to work.

What To Watch

The Century Foundation flagged the bigger picture in a report this week titled "When the Wheels Come Off."

Its authors warned that high auto costs and rates are pushing record numbers of borrowers into longer loans, which keeps households trapped in debt. Their line worth repeating: "Paradoxically it is low-income borrowers, with the least disposable income, that carry the most auto loan debt."

The Fed has held rates higher for longer, and the bottom half of borrowers is now showing the strain.

If you want this kind of read on the market every morning, join 350,000+ investors getting Market Briefs - plus a free 45-minute investing masterclass as a bonus.