South Korea's AI chip boom just got more complex.

The country's biggest chipmakers are paying workers hundreds of thousands of dollars in bonuses. That cash is flooding the housing market.

And the Bank of Korea is now trying to figure out what to do about it.

The Pay Packages Are Massive

Samsung and its union agreed on May 20 to a new pay deal for chip workers. The deal stacks two big perks.

The bonus is tied to about 10% of chip profit. That could mean up to 600 million won (around $400,000) per worker this year.

The new deal builds on a tentative wage deal Samsung struck last year that headed off a long strike.

There's also a low-rate home loan, with rates set at 1.5% for 10 years. Workers can borrow up to 500 million won (around $370,000) for a home.

SK Hynix has its own version. Payouts there are set to average $460,000 to $477,000 per worker this year, across the firm's 35,000 staff.

We track macro stories like this every morning in Market Briefs. Five-minute reads sent before the market opens, plus a free investing masterclass when you join.

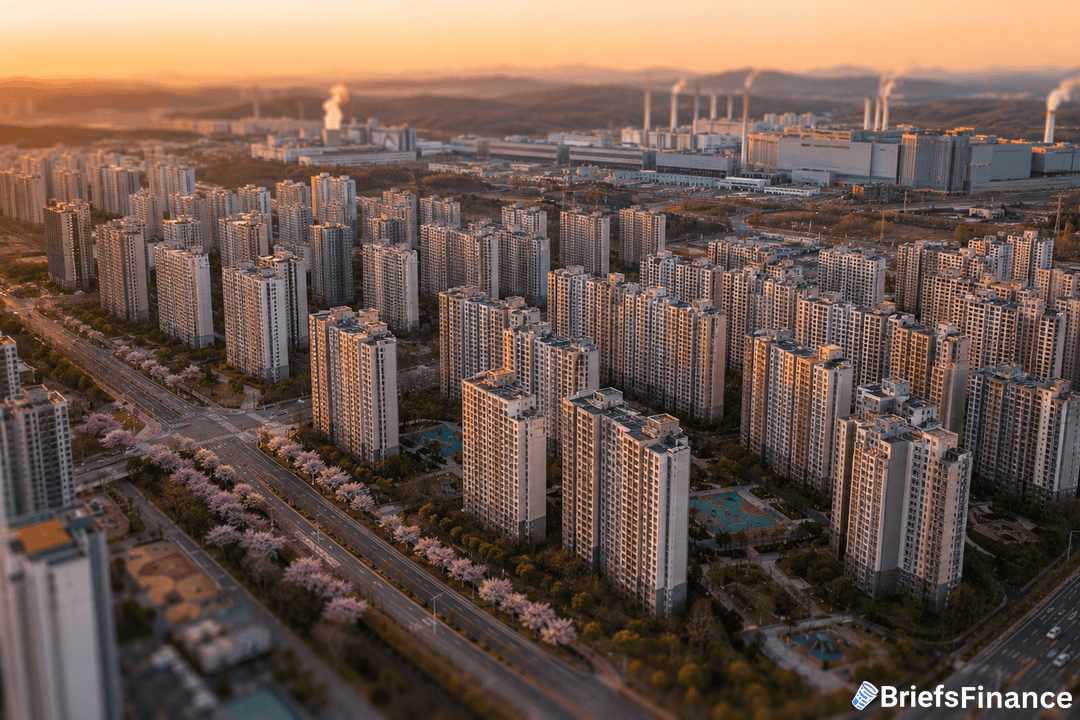

The Housing Market Already Sees It

The cash hasn't even hit bank accounts yet. Home prices in the "chip belt" are already jumping.

The chip belt is the zone around Samsung and SK Hynix sites. That's where most chip workers live.

Weekly price gains in mid-May, per the Korea Real Estate Board:

- Yongin Suji: up 0.38%

- Suwon Yeongtong: up 0.35%

- Hwaseong Dongtan: up 0.49%

Those gains are speeding up. Dongtan has been hitting record home sale prices, with one 84-square-meter unit selling for 2.08 billion won on May 7.

These zip codes sit on shuttle routes for the chip giants. The pay raise is showing up in home prices before it shows up in paychecks.

Why The BOK Is Watching

Bloomberg Economics says this stops being a labor story. It becomes a macro one.

When you funnel that much cash into a small set of zip codes, three things happen at once. Home prices rise. Spending rises. Wage pressure in other jobs rises.

That's the setup for sticky inflation. Korea's inflation has been running above 2.2%.

Growth has tracked at or above 2% since April. The central bank has lifted its 2026 growth view to 2%.

Top BOK deputy Ryoo Sang-dai said this month it's time to think about hikes. That would be a turn for a bank that's been on hold at 2.5%.

Korea is matching the pattern in Europe. Banks that were cutting are now turning back to hikes.

What To Watch

The BOK's next meeting will set the tone. A hawkish pivot would be a big shift for Asia's fourth-largest economy.

For investors, the bigger story is the link between AI chip profits and the Korean economy. Samsung and SK Hynix don't just sell chips.

They now move housing, inflation, and policy in one country at once. That's a level of clout most economies don't price in.

If you want to see how moves like this hit the market, join Market Briefs. Daily reads every weekday morning, and you'll get a 45-minute course on finding investments as a thank-you.