Housing markets often swing one way or the other. Right now, they are doing something stranger.

Inventory is up, prices are softer, and homes are still moving. None of those should be true at the same time.

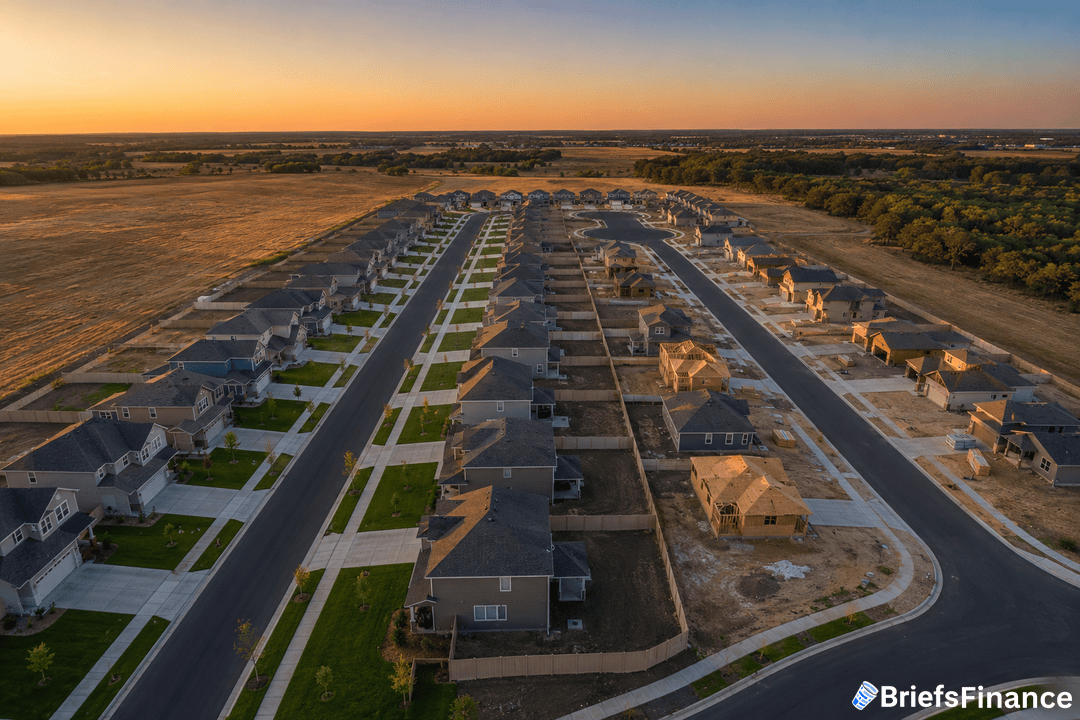

That balance shows up clearly in Realtor.com's latest weekly read, where new listings sit near their highest level in nearly a year.

The Numbers Tell Two Stories

Buyers are soaking up new listings at about the same pace as last spring. The result is a quiet tug-of-war between supply and demand.

On the supply side, things are loosening up.

National inventory is up 2.3% from a year ago, while median list prices are down 2.2%.

About 36% of active listings have had at least one price cut. That is a sign sellers are still chasing the market rather than leading it.

Buyers should love that. Most do not, because the math at the closing table still does not work.

The 30-year fixed mortgage rate just climbed back to 6.45%, the highest in a month, after sitting at 6.37% the week before.

Mortgage applications fell 4.4% week over week as a result.

The national median monthly payment for new buyers also jumped to $2,131 in March, up from $2,061 in February.

NAR data shows home prices rose in 71% of metro areas in the first quarter, with the median single-family price up 0.5% year over year to $404,300.

Even with that small bump, growth has cooled from the 1.2% yearly gain seen in late 2025. The heat is leaving the bidding floor.

Why Homes Are Still Selling

Despite the squeeze, pending home sales just hit their highest level in nearly four years. That is not a typo.

A big chunk of the answer is new builds. Builders sold 682,000 newly built homes in March. That was up 7.4% from February, and new home prices fell to a five-year low.

Why? Builders can buy down rates and trim prices in ways most sellers cannot.

The other piece is patience finally cracking. Buyers who sat out 2023 and 2024 are now five years deep into waiting.

Redfin reported that buyers leaned in last week as rates briefly dipped, even as the broader spring run is still tracking slower than past years.

Even with that nudge, the spring market is still running well behind the pace of 2021 or 2022.

What To Watch

The spring window is the real test. The next few weeks will show how much pricing power sellers actually have left.

If rates hold near 6.45% and inventory keeps climbing, sellers will have to choose between cutting prices harder or sitting on listings into the summer.

Builders will likely keep pulling demand toward new homes, mostly in the Sun Belt where they have the most room to discount.

Liquidity is back in the housing market for the first time in years.

Affordability is still missing in action.

That gap is the real story of spring 2026 for both buyers and sellers.