Home inspections are quietly changing how homes get bought, sold, and financed in 2026. A new HousingWire report highlights four shifts reshaping the inspection business, each one pointing to a more buyer-friendly market than the 2021-2022 peak.

The changes also give lenders a clearer view of collateral, which matters when credit standards are tightening across most of the country.

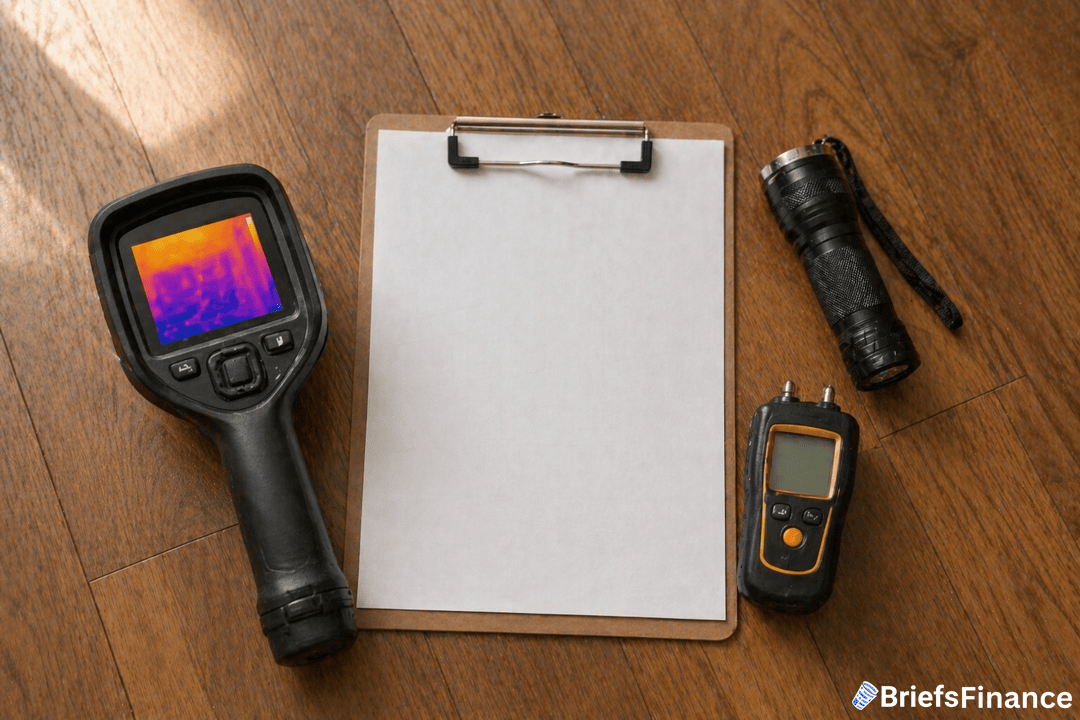

Thermal Imaging Goes Mainstream

Five years ago, thermal imaging was a luxury add-on that inspectors charged extra for. Now it is becoming baseline, because infrared technology shows missing insulation, air leakage, moisture intrusion, and hidden electrical hotspots long before those issues become visible.

The benefit flows beyond the buyer to lenders, who see fewer post-closing defect claims when thermal imaging is done upfront. That protects collateral value and reduces early payment defaults tied to surprise repair bills.

11-Month Warranty Inspections Grow

New homeowners are increasingly hiring inspectors 11 months after closing, right before the builder's standard one-year warranty expires. That lets the homeowner formally document defects before losing their recourse with the builder.

Where it is standard: the service has become routine in hot Texas markets like Kyle, San Marcos, and Buda, where new construction volumes are high and warranty disputes have become common.

The shift also pulls more year-round revenue into a business that used to be heavily seasonal.

Buyers Stop Waiving Inspections

At the peak of the 2021-2022 housing frenzy, waiving the inspection was common, because sellers could demand it in multi-offer bidding wars. As competition cools, that is going away, and buyers are using their negotiating leverage to put inspections back on the table.

That changes how lenders, agents, and buyers manage due diligence and timelines. Deals take slightly longer, but the collateral is better understood before funding, which tends to lead to better pricing decisions on both sides.

What It Means for the Industry

Inspectors are seeing fuller schedules, steadier year-round work, and more competition from new entrants. Positioning and service offerings matter more than ever, so companies that invest in AI-assisted reports and thermal imaging have an edge over cheaper, less thorough competitors.

Software companies serving inspectors are also growing faster, as buyers expect digital reports and photo evidence inside one platform.

The Insurance Connection

Insurers are also leaning on better inspection data, especially after three years of climate-driven claim spikes. Carriers are quietly using inspection reports to price individual homes more accurately, especially in wildfire and hurricane zones.

That tightens the loop between inspections, mortgage pricing, and insurance premiums into a single information stack. Buyers who invest in a thorough inspection up front increasingly get better insurance terms down the line.

What to Watch

The next test is whether this rising standard shows up in appraisal data. If lenders start using thermal imaging and inspection data to re-rate collateral, the cost of financing could start to reflect inspection quality.

That would be the first real feedback loop between home inspections and mortgage pricing.