The headline number on Cheniere's first quarter is brutal: a $3.5 billion net loss against a $353 million profit a year ago. The cash flow picture is the opposite, with record exports, EBITDA up 25%, and raised full-year guidance.

Both pictures are accurate, and the gap between them is the entire story.

The Loss Is An Accounting Story

Cheniere sells natural gas and buys it through long-term agreements that get marked to market every quarter, so when global gas prices swing, the value of those contracts swings with them on paper.

The Iran war broke open Middle East gas supply, sending international gas prices and price swings sharply higher. That move pushed up the future cost of the gas Cheniere has agreed to buy, and the company had to take a $5.4 billion non-cash mark on those positions.

Strip out that mark and adjusted net income was $1.0 billion, up from $794 million the year before. The bottom line: the cash this quarter went the right direction, even though the GAAP line did not.

Distributable cash flow came in at $1.67 billion for the quarter, and the company raised full-year DCF guidance to a range of $4.75 billion to $5.25 billion - up from a prior $4.35 billion to $4.85 billion.

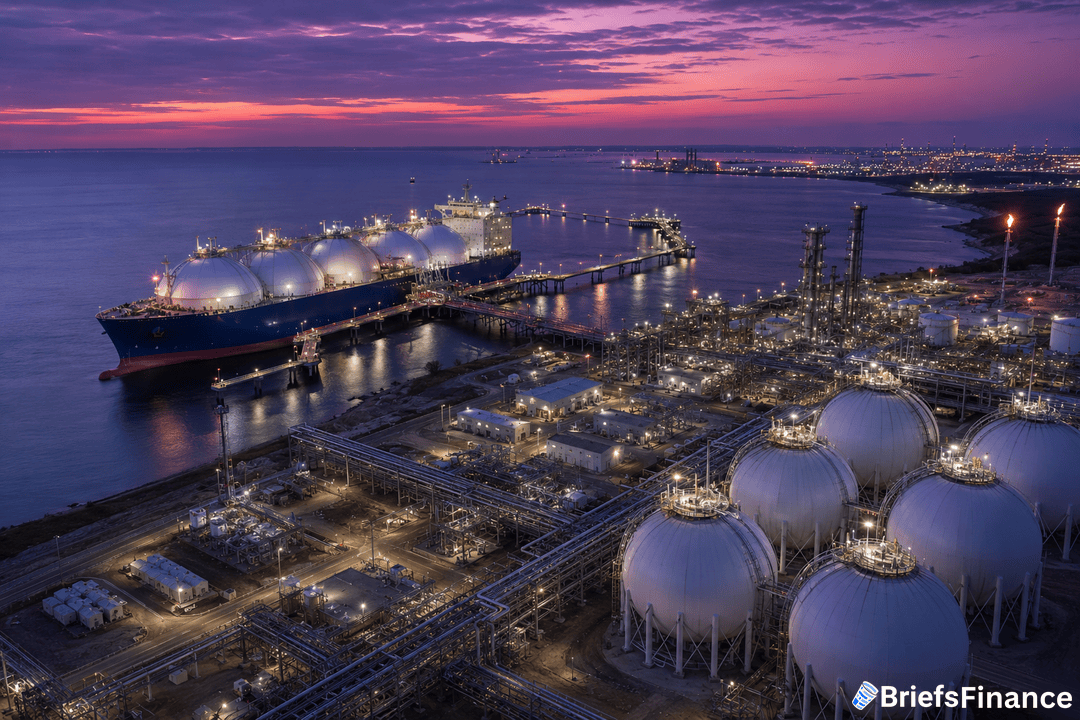

The Operating Side Is Booming

Volumes did the heavy lifting, with Cheniere shipping 187 LNG cargoes in the quarter - a record. Total LNG volumes loaded rose 13% to 688 trillion British thermal units.

The Middle East disruption is good for U.S. exporters, since the closed Strait of Hormuz and damage at QatarEnergy's Ras Laffan facility took roughly 7 million tonnes of monthly Middle East LNG supply offline. Cheniere said on its earnings call it expects the global LNG market to stay structurally tight through 2027.

That tight market is showing up in margins, with the company saying open capacity for 2027 was selling at margins under $4 in February. Today those same volumes are clearing closer to $6 or $7.

Cheniere also kept returning cash to shareholders, repurchasing about 2.7 million shares for $537 million in the quarter and paying a dividend of 55.5 cents a share.

What To Watch

CEO Jack Fusco said the volatility "further signals the need for additional investment in reliable, secure LNG capacity." Translation: Cheniere plans to keep building.

The Corpus Christi Stage 3 expansion is 96.5% done, with Train 5 reaching substantial completion in March and first gas from Train 6 expected imminently. Trains 6 and 7 are expected to reach substantial completion by year-end.

The next quarter will tell investors whether the IPM contract marks reverse out as gas prices stabilize. That's the only piece of this story that can flip the loss number back to a profit on paper.