The ceasefire just got an extension. The blockade didn't.

Trump announced Tuesday that the two-week US pause in the Iran conflict will continue, hours before it was set to run out. He pointed to Iran's "seriously fractured" government as the reason. He also said the US Navy will keep its blockade of Iranian shipping ports in place.

We're now on day 52 of the Middle East conflict. The initial ceasefire dropped April 7.

What The Extension Actually Means

Trump said the pause holds until Iran submits a "unified proposal" to end the war. That's the diplomatic version of "call me when your team agrees on the offer."

The sticking point is Tehran itself. Vice President JD Vance's trip to Pakistan for the next round of talks got put on hold. Iranian state media reported that negotiators told the US, through a Pakistani intermediary, that they won't be showing up to further talks for now.

So the war isn't restarting. But nothing's actually getting resolved either.

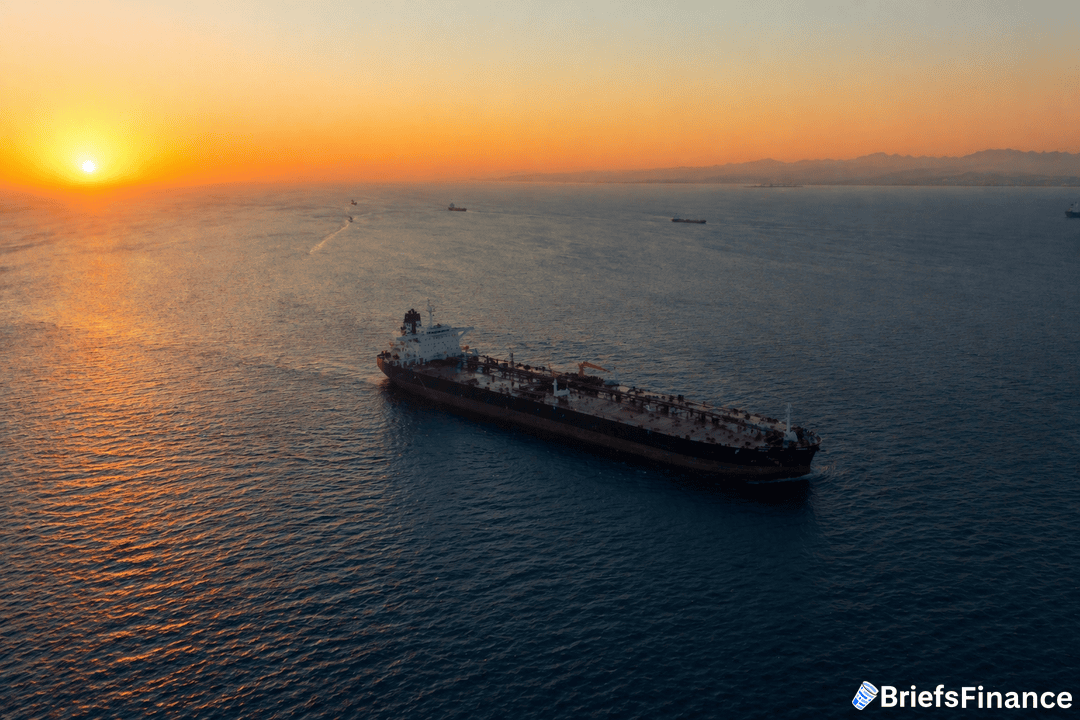

Why The Markets Actually Care

The Strait of Hormuz moves about 20% of the world's seaborne oil. The blockade, even a soft one, keeps traders nervous about shipping. That nervousness is why crude jumped 30% last quarter, gasoline was up 24% in March, and Alaska Airlines just pulled its full-year forecast this morning.

An extended ceasefire takes the worst-case scenario off the table for a few more weeks. It doesn't take the Hormuz risk off the table. That risk is now priced into every airline, freight, and chemical stock investors hold.

The Hormuz Read-Through

The Strait of Hormuz carries about 20% of the world's seaborne oil, which means anything that slows traffic through that lane lifts the global crude price within hours. The US blockade doesn't have to stop ships to move the market. It just has to keep the insurance premium on every tanker route nearby elevated.

Those higher shipping insurance costs show up in three sectors first. Airlines see it in jet fuel, which is why Alaska pulled its guide this morning. Chemicals companies see it through naphtha and petrochemical feedstocks. Freight sees it in the bunker fuel bill.

Think of the Hormuz risk as a tax that gets added to every cargo moving through the Gulf until the blockade comes off. Traders aren't trying to guess when it lifts. They're just pricing the tax.

That tax also lands on consumer staples. Packaged goods makers run oil-based inputs through every line item, which is why producers of food, cleaning products, and plastics are marked lower as long as crude stays elevated on Hormuz headlines.

Chemicals and refiners show the cleanest signal. When crude spikes and stays, input costs climb for anyone running a cracker or a distillation tower, and margins compress until retail prices catch up two or three quarters later.

Worth Noting

The next trigger is Vance's Pakistan trip. If it gets rescheduled, markets will read that as progress. If Iran refuses to send negotiators again, the blockade tightens and oil reprices higher.

Either outcome shows up at the pump first.