The BOJ kept rates on hold at its last meeting, but the Summary of Opinions released today says the next move is coming fast.

Three of nine board members pushed for an immediate hike, and the bigger surprise is that Iran is making the case for them.

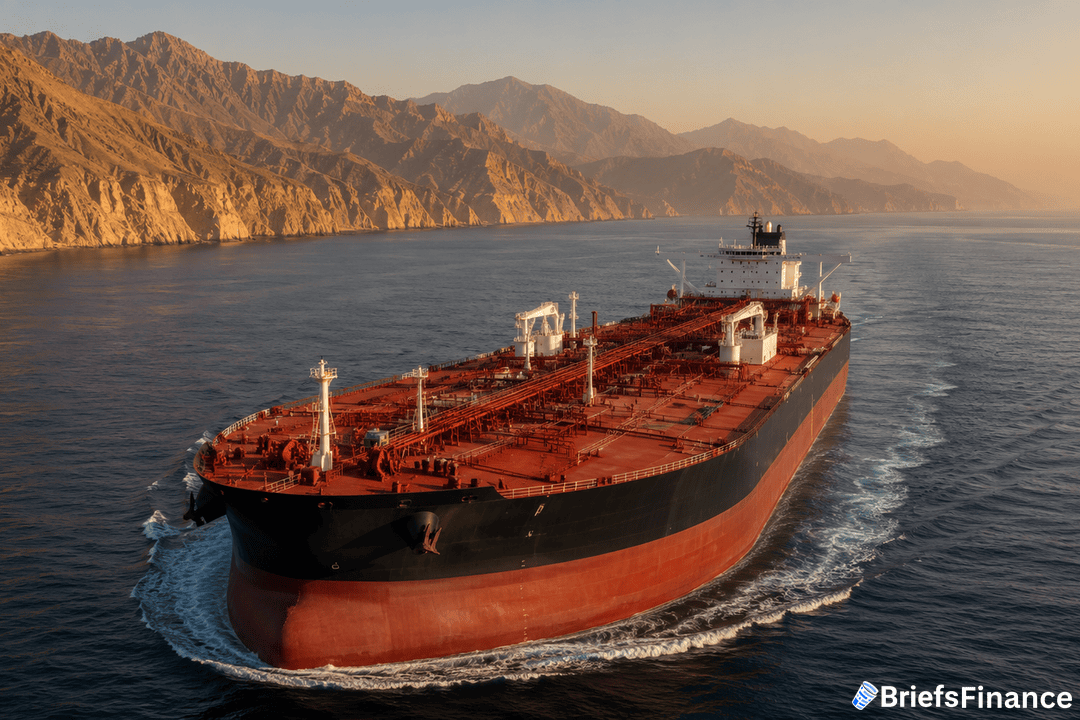

How Iran Is Driving Japan's Inflation

Japan imports more than 90% of its crude oil from the Middle East, which puts the Strait of Hormuz at the center of Japan's inflation problem. The shipping lane handles roughly one in every five barrels of oil and gas traded worldwide.

The Iran war has slowed that flow since the fighting started, lifting crude prices and forcing Japan to pay more for every shipment.

Energy costs are rising while the yen stays weak, a combination that makes every imported barrel more expensive in yen terms and pushes prices up faster than the BOJ wants.

The bank lifted its FY2026 core inflation forecast to 2.8% from 1.9% in the same April meeting, a big jump in a single quarter.

We unpack what moves like this mean for your portfolio every morning in Market Briefs, and new readers get a 45-minute investing masterclass as a free bonus.

The Board Is Splitting

Three of the BOJ's nine board members called for a hike at the April 27-28 meeting, while the other six voted to wait.

One member put it plainly in today's summary: it is "quite possible" the BOJ will raise rates at the next meeting even if the Middle East stays unstable. Another said the bank should hike "without hesitation" if inflation risks keep climbing.

That tone is a shift for a bank known for moving slowly. Japan kept its policy rate at or below zero for most of the past decade before starting to nudge higher last year.

The catch: the BOJ is also dealing with soft growth. The same April meeting trimmed the FY2026 growth forecast to 0.5% from 1.0%, which is usually the kind of backdrop that argues for keeping rates low, not raising them.

What To Watch

The next BOJ meeting is June 15-16, and Japan's inflation has run above the bank's 2% target for four years now. The April forecast says it will stay there.

A June hike would put real pressure on the yen carry trade, which is the strategy of borrowing cheap yen to buy higher-paying assets in other markets. Trillions of dollars sit in versions of that trade across US Treasuries, emerging market debt, and global stocks.

For US investors, the most direct effect would land in Treasury yields, since Japanese institutional buyers hold a huge slice of US government debt. A tighter BOJ tends to pull some of that money home.

Japanese banks usually rally on hike news because they make more on lending, while exporters often fall on a stronger yen. The TOPIX index, Japan's broad stock benchmark, tends to reflect both pulls.

After years of being the slowest major central bank to tighten, the BOJ may finally move because of Iran.

If you want this kind of read on global rates every morning, join Market Briefs - the investing course comes with the signup at no cost.