Saudi Arabia has two ways to fix a tight budget. It can pump more oil. Or it can wait for prices to rise.

Brent is up. Saudi cannot ship enough barrels to take advantage. The Hormuz blockade caps how much oil the Kingdom can move out.

So the volume hit is what is breaking the budget.

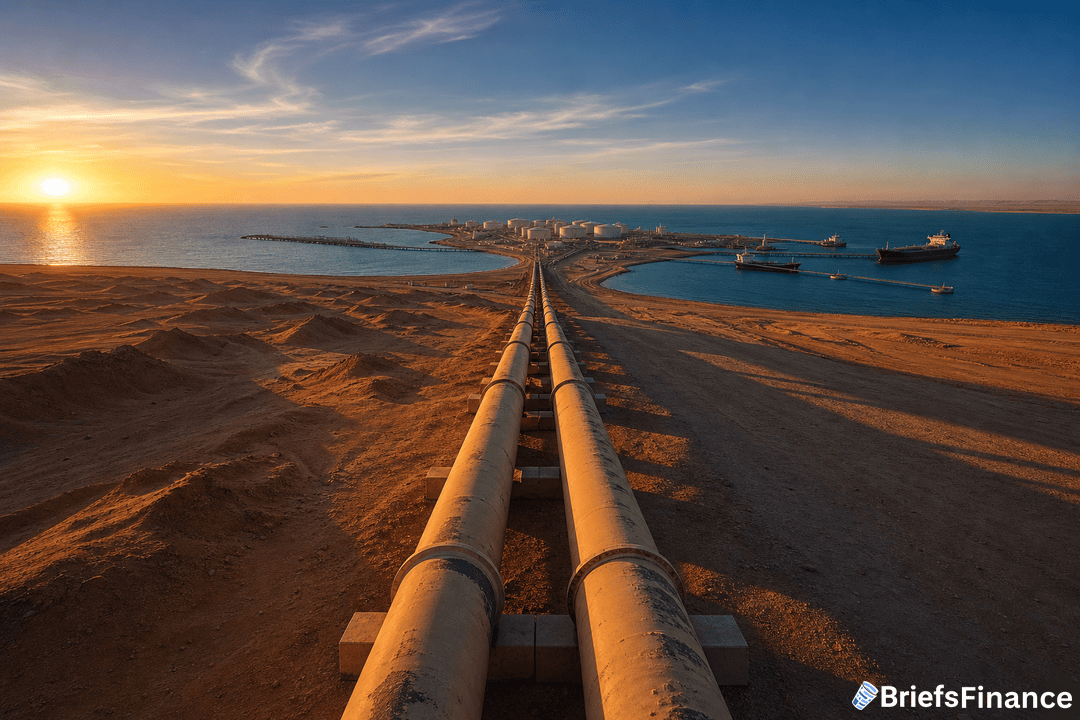

The 5 Million Barrel Cap

Saudi Arabia has only one working oil export route. The East-West pipeline runs from the Eastern Province to Yanbu on the Red Sea coast.

The pipeline can move about 7 million barrels a day at full tilt. Local refineries soak up about 2 million of that.

That leaves a hard cap of 5 million barrels for export. The Kingdom's OPEC+ quota is 10.2 million.

So half of Saudi Arabia's allowed output has nowhere to go. That stays true even if Riyadh wanted to flood the market.

The shipping data shows the squeeze. Saudi Aramco cut crude supply to Asian buyers by almost 39% from February to March, with shipments dropping from 7.1 million barrels a day down to 4.4 million.

The Breakeven Math

The IMF puts Saudi Arabia's fiscal breakeven at $86.60 a barrel. That is the oil price the Kingdom needs to balance the books.

Bloomberg Economics says the real number is closer to $94. That is once Public Investment Fund spending is added in.

With full PIF spending, the number climbs above $110.

Brent has been volatile, falling as low as $65 in early April before climbing back above $113 by early May. Higher prices help, but the Yanbu cap means Saudi cannot ship enough barrels to fully capture them.

Riyadh entered 2026 with a borrowing plan of about $58 billion. That plan was sized for a world where Hormuz was open.

The plan now looks too small. Goldman Sachs pegs the real deficit at 6 to 6.6% of GDP. That works out to roughly $80 to $90 billion.

Vision 2030 Megaprojects Slow

The big projects that define Vision 2030 were built around $250 billion of yearly oil money. NEOM, the Red Sea Project, and New Murabba all sit inside that pipeline.

None of those projects pencil out with capped exports and ongoing budget gaps. NEOM's The Line was paused in September 2025 with just 2.4 of its planned 170 kilometers built.

The Red Sea Project is also slowing builds by year-end. PIF's liquid cash had fallen to about $15 billion by late 2024, the lowest level in years.

Aramco then cut its 2025 dividend by about a third to $84.5 billion. That cut directly trimmed PIF's income.

What To Watch

Saudi Arabia entered 2026 with $438 billion in foreign cash reserves. That sounds like a lot.

The Kingdom burned through $109 billion of those reserves in under a year during the 2015 oil crash. It could still export at full capacity back then.

This time it cannot. The Yanbu cap is the new ceiling, and it does not lift on its own.

Saudi sovereign debt is also already past $300 billion. The pre-crisis plan put it on a path toward $350 billion by year-end.

Aramco's 2025 dividend cut and the slow pace at NEOM both add to the squeeze. Vision 2030 was the long bet. The short-term cash question is now more urgent.