The first group born into texting now has a real-estate footprint. It does not look much like the one their older siblings left behind.

Gen Z is everywhere in Minneapolis. They are almost nowhere in Miami.

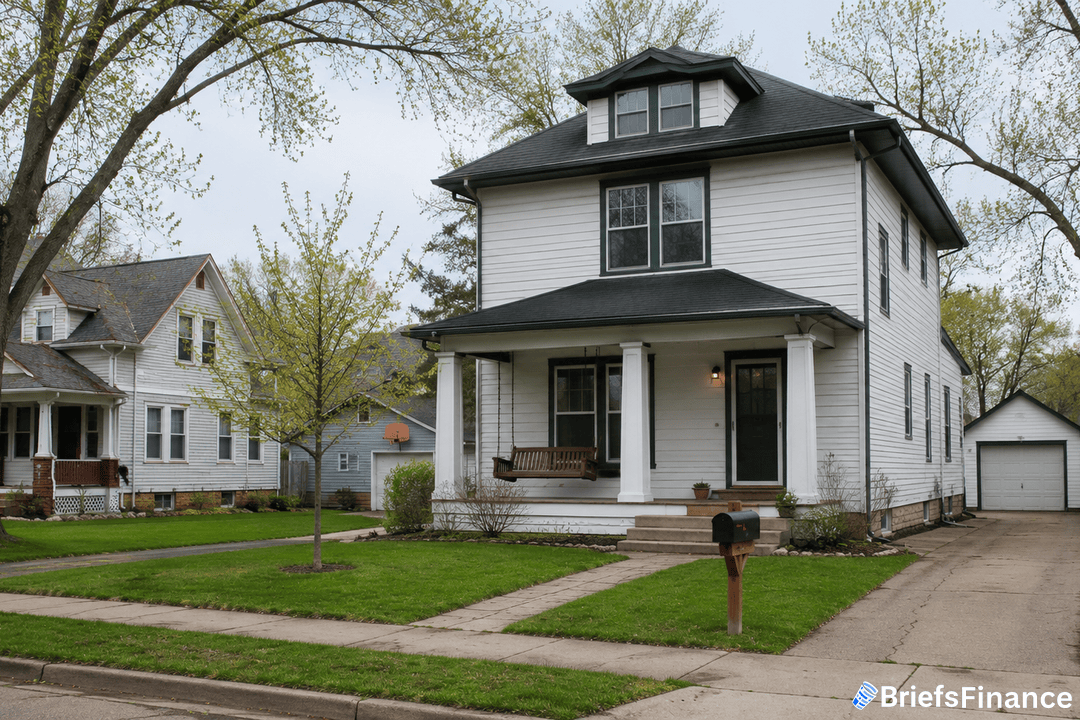

The Map Looks Midwestern

Across the 50 biggest U.S. metros, Gen Z makes up about 20% of mortgage buy requests. That is per a new look from LendingTree at home buy data from 2024 through 2025.

Gen Z buyers are defined here as adults age 18 to 28 in 2025.

The strongest Gen Z share sits in the middle of the country:

- Minneapolis: 26.4%

- Birmingham, AL: 25.7%

- Indianapolis: 24.6%

The shared thread is what a home costs. Down payments are smaller, loans are smaller, and the math works for a 25-year-old with a starter job.

Minneapolis also has high credit scores across the state, which gives buyers more room with lenders.

Every morning, Market Briefs breaks down how shifts like this move markets - in five minutes, plus a free investing masterclass when you sign up.

The Coasts Don't Show Up

The bottom of the list is the inverse of the top. Miami, San Francisco, and Las Vegas have the smallest Gen Z share, all under 13%.

San Francisco's average loan request is $621,577, and the average Gen Z down payment there is $140,005. That math does not work for someone in their mid-twenties.

Gen Z buy activity did jump 33.9% in San Francisco from 2024 to 2025, so they are trying. They are just not closing the same way they would in St. Paul.

Six metros lost Gen Z share altogether. Miami led the drop at -10.5%, with Portland and Orlando close behind.

Why It Is Happening Now

LendingTree's Matt Schulz pointed to a side effect of high mortgage rates. Older owners with low-rate loans are not moving, which leaves more room for first-time buyers - and a lot of those buyers are Gen Z.

In plain terms, the rate lock-in that froze the move-up market is doing Gen Z a favor on the entry side.

That dynamic is showing up in growth numbers too. Virginia Beach saw the biggest jump in Gen Z mortgage share from 2024 to 2025 at 37.1%, with Birmingham close behind at 30.9%.

Schulz also flagged a credit-score angle. Areas with higher average credit scores tend to clear lenders more easily. That helps places like Minneapolis even when the price tag is not the lowest on the map.

Worth Noting

Millennials still run the housing market. They made up 40.5% of mortgage buy requests in 2025, with Gen X next at 26.3%, Gen Z at 19.9%, and Boomers last at 12.7%.

What sets the Gen Z slice apart is the size of the check.

The average Gen Z down payment is $44,966, and the average Gen Z loan is $274,794. Millennials are putting down $72,412 on average and borrowing $356,655.

That is roughly $80,000 more in loan size than the Gen Z buyer next door.

Housing demand is not dying. It is quietly moving inland.

If you want this kind of read on the market every morning, sign up for Market Briefs here - it comes with a free 45-minute investing course as a bonus.