Restaurant CEOs aren't usually the ones describing how much gas costs.

This earnings season they are, and it's because the gap between what high earners and low earners do at the pump just got wider.

The CEO Warnings

Executives across retail, restaurants, and packaged goods are flagging the same trend, with budgets tighter, spending softer, and pump prices doing most of the damage.

Kraft Heinz's CEO said shoppers are "literally running out of money toward the end of the month."

McDonald's CEO Chris Kempczinski called the environment "challenging" on the Q1 call, adding that it isn't improving and may be getting worse.

Domino's and Chipotle reported sales softening in March, right after the Iran war started, which lines up with the broader pattern.

Strip out the company names, and the message is the same across the food and packaged goods space: the low-end consumer is pulling back.

The K-Shape Is Back At The Pump

Research from the Federal Reserve Bank of New York spelled out the split.

When pump prices spiked in March, households making less than $40,000 lifted what they spent on gas by only 12%, and they did it by driving 7% less.

Households making more than $125,000 spent 19% more and barely cut back, with consumption down just 1%.

That's the K-shape pattern economists have flagged since the pandemic, where higher earners ride out price shocks while lower earners absorb them.

Energy prices have climbed 56% in the post-pandemic economy, per the New York Fed, and wages at the low end haven't kept up.

For an investor lens, that means restaurant traffic, dollar stores, and packaged goods aimed at lower-income shoppers carry the most direct exposure to a long gas spike, while premium retail has more cushion.

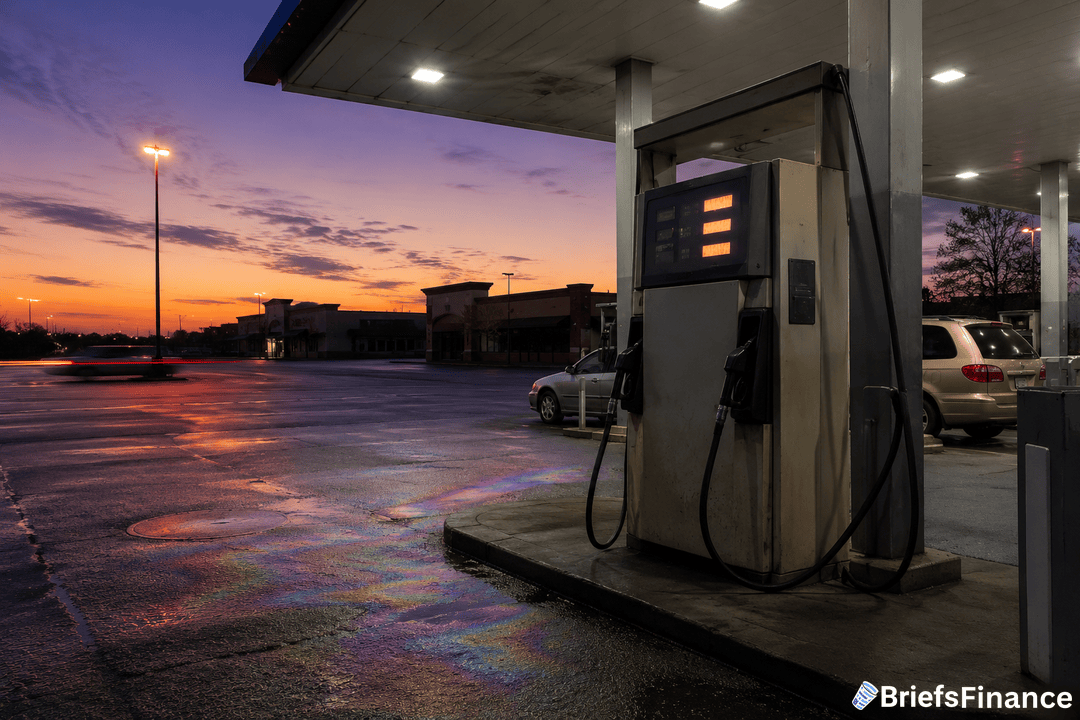

How Big Is The Squeeze

The national average gas price hit $4.48 a gallon, up from $4.18 a week earlier, which puts pump prices within reach of the all-time AAA record of $5.02 set in June 2022.

California's average is already $5.97, and the price has risen 11% in under two weeks.

Bank of America Institute data shows the median lower-income household spent 4.2% of its income on gasoline in March, up from 3.9% a year earlier.

JPMorgan Chase data showed driving levels in March and April trending slightly lower than last year, an early signal that high-frequency travel is bending.

Wages aren't keeping up either, since wages and salaries grew just 1% for low-income households in March, against 5.6% at the high end, per Bank of America.

What To Watch

Chevron CEO Mike Wirth told CBS's Face the Nation that gas prices haven't peaked for the year, citing the war and the Strait of Hormuz closure.

Investors should watch May same-store sales reports from low-end restaurant and dollar-store names, since that's where the squeeze hits the income statement first.

The next round of credit-card data and consumer confidence prints will also matter, since lower-income households tend to lean on credit when paychecks fall short.

If gas prints break the 2022 record of $5.02 a gallon, the political pressure on Washington to find a way out of the war will grow on top of the economic pressure already on consumers.

That's where this story gets harder for both retailers and policymakers.