China's first quarter GDP grew 5%, putting the economy on track for its 2026 target. April reversed that picture, with retail spending, factory output, and investment all missing forecasts as the Iran war piled onto a still-weak property market.

April Data Missed Across The Board

Retail sales rose just 0.2% from a year earlier in April, far below the 2% economists expected and a sharp slowdown from 1.7% growth in March. That was the weakest consumer spending in China since December 2022.

Factory output came in at 4.1% year-on-year growth, the slowest pace since July 2023 and well short of the 5.9% forecast. The number pointed to softer demand at home pressing on order books.

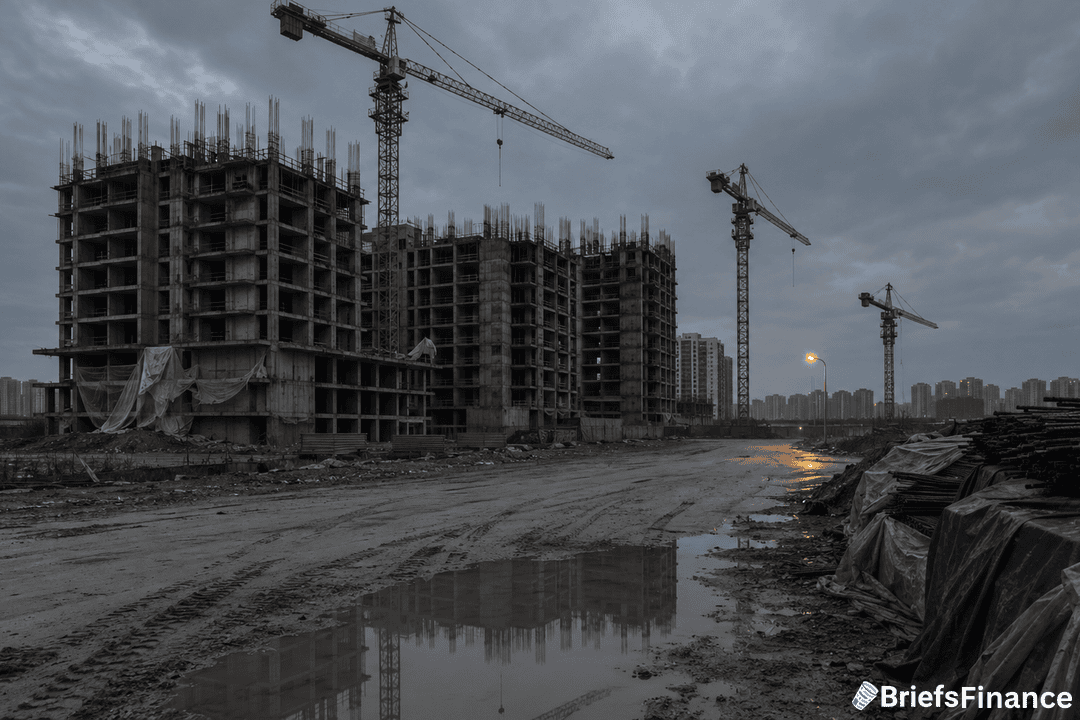

Fixed-asset investment - the money China spends on roads, factories, and property - swung from 1.7% growth in Q1 to a 1.6% drop through April. That flagged a pullback in both construction and infrastructure at the same time.

April auto sales fell 21.6% from a year earlier, the seventh straight month of declines, even as Chinese carmakers push harder overseas to make up for weak demand at home.

Chinese consumer confidence indexes have been stuck below pre-2022 levels for almost three years, even after the central bank's rate cuts and a string of housing support measures.

The macro reads that actually move portfolios get broken down every morning in Market Briefs - five minutes a day, with a free investing masterclass thrown in when you sign up.

Iran's War Is Pressuring Both Sides Of The Economy

Beijing's National Bureau of Statistics flagged heavy rainfall in southern China, slower construction, and the still-shaky property market. The bigger weight is sitting in the Middle East.

The Iran war has pushed energy costs higher and weighed on global trade, hitting China hardest because it's the world's biggest oil importer. When crude moves, factory margins and consumer wallets move with it.

The property market is still the open wound, with households watching home prices go sideways or down and pulling back on spending. That keeps retail soft and factories cautious about adding capacity.

For global investors, weaker Chinese demand is a problem because China is the biggest buyer of copper, iron ore, and oil. A slowdown in Chinese activity has historically dragged commodity prices down with it.

What To Watch

Beijing has plenty of policy tools left, including rate cuts, infrastructure spending, and easier credit for local governments. The question is whether it pulls the trigger fast enough to keep 2026 on track for its 5% growth target.

The next big data point is May retail sales, due in mid-June, along with any signal from the People's Bank of China on rates. Those two prints will set the tone for whether April was a one-month blip or the start of a slower second half.

If April turns out to be the new pace, the central bank's next move gets a lot more interesting.

If you want this kind of read on what's actually moving global markets, join the 350,000+ investors reading Market Briefs - you also get a free 45-minute investing course when you join.